of Iron

War is typically narrated through the language of the map room. We track front lines and territorial shifts, parse the communiques of foreign ministers, and follow the movements of naval task forces. The map has an obvious appeal: it is immediate, legible, and dramatic. What it consistently obscures is the deeper contest that determines whether any military campaign can be sustained at all. That contest is economic. It always has been.

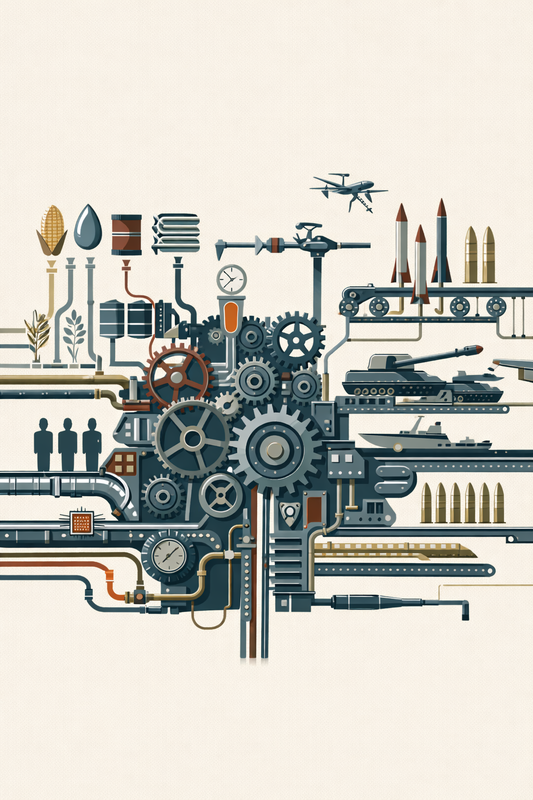

In peacetime, economies are organised around a particular logic: the pursuit of consumer demand, the optimisation of just-in-time supply chains, and the compounding of civilian prosperity. Factories produce vehicles and appliances. Capital flows toward the highest available return. It is a logic of abundance, and it is extraordinarily efficient at what it does. Conflict destroys this logic. The classical trade-off between guns and butter, which economic textbooks treat as a tidy abstraction, is in practice a violent redirection of national capacity. It is the moment a government decides that a shipment of steel is more valuable as armour than as a bridge. It is the moment an engineer's expertise is reassigned from oncology imaging to ballistic guidance. This is not a marginal adjustment. It is a civilisational pivot from prosperity to survival.

War may be triggered by politics and fought by soldiers. It is sustained, won, or lost through the relentless arithmetic of the economy.

The Meridian · April 2026History is blunt on this point. The Second World War was not decided by superior generalship alone. It was decided by the scale and tempo of industrial output. Automobile plants became aircraft factories. Shipyards launched vessels at a rate that remains statistically staggering. The Allied mobilisation represented the largest coordinated industrial effort in recorded history, and its central lesson has never been safely forgotten: in a prolonged conflict, the ultimate arbiter is not the soldier in the field but the factory floor behind him.

In 2026, the machinery of war has evolved considerably, though its dependencies have not disappeared. Napoleon's observation that an army marches on its stomach was a recognition of logistics as the binding constraint of military power. Today that constraint has multiplied in complexity. A modern force requires semiconductors, satellite constellations, persistent data infrastructure, and access to globalised energy networks. If any one of these supply chains falters, the most sophisticated hardware in the inventory becomes inert. This edition looks past the front-page narrative to examine the structural foundations on which the entire enterprise rests.

We begin with the military-industrial complex as a distinct economic sector, because it no longer functions as one. The 21st-century defence economy is characterised by a deep and largely irreversible integration with the civilian technology sector. The emergence of what analysts are calling the algorithmic front has placed major technology firms at the centre of military planning, not as suppliers of peripheral equipment but as architects of operational capability. Data analytics, artificial intelligence, and private intelligence markets have created a new economics of warfare in which information itself is a high-yield strategic commodity.

Global defence expenditure crossed $2.4 trillion in 2025, the highest figure in recorded history. Across the G7, the average ratio of defence spending to GDP is rising for the fourth consecutive year. The fiscal implications of this structural shift extend well beyond the defence sector itself.

If industry provides the hardware of war, finance provides its oxygen. The question of who pays, and on what terms, is rarely glamorous. It is nonetheless decisive. Whether through sovereign debt issuance, emergency taxation, or the subtler mechanism of financial repression, the fiscal cost of modern warfare is reshaping national budgets across the globe in ways that will outlast the conflicts that generated them.

As global military expenditure rises, the macroeconomic implications are compounding. Higher defence budgets crowd out private investment, erode fiscal guardrails, and create structural pressures on social spending that accumulate quietly until they cannot be ignored. We also examine the growing role of financial sanctions as an instrument of coercive statecraft. In an integrated global economy, the capacity to sever a state from the international payments system carries a destructive force comparable to a conventional military strike. And yet, as our investigation into what we have called the shell game reveals, these measures have simultaneously given rise to sophisticated circumvention networks. States and non-state actors are increasingly routing transactions through digital currencies, commodity swap arrangements, and informal settlement systems that sit entirely outside the reach of Western financial institutions. This shadow economy is not a peripheral curiosity. It is becoming a central pillar of wartime economic survival.

No economy escapes its physical limits indefinitely. In our March edition, we examined the structural constraints on growth in peacetime. In April, we apply that same lens to conflict. Modern weapons systems are voracious consumers of specific materials. Rare earth elements, lithium, and cobalt are no longer merely inputs for the green transition; they are strategic minerals in the most classical sense of the term. Without them, there are no precision-guided munitions, no advanced communications systems, and no sovereign capability in the technologies that now define military competition. The struggle to secure and control these resources is already reshaping trade flows and diplomatic alignments, particularly across the Global South, where the relevant deposits are concentrated.

Energy remains the primary lubricant of military mobilisation. We analyse the continuing centrality of oil and gas, alongside the accelerating vulnerability of electricity infrastructure to cyber operations. War's disruption of agricultural supply chains and water security does not remain confined to the theatre of conflict. It creates feedback loops of civil instability, displacement, and secondary violence that extend far beyond any front line. When water infrastructure is destroyed and food systems collapse, the resulting mass migration becomes not merely a humanitarian catastrophe but a further driver of geopolitical disorder.

For the Global South, the return of the war economy is not a distant geopolitical development to be observed from a safe remove. It is a structural pressure landing directly on national budgets, development trajectories, and the political calculations of governments already managing fragile fiscal positions. Across the Sahel, surging security expenditure is crowding out the public investment that development frameworks depend upon. In Sudan, the political economy of gold continues to fuel a devastating internal conflict in which the incentive to sustain the war is inseparable from the incentive to control the revenue. In the Indo-Pacific, naval expansion is forcing governments to make explicit trade-offs between maritime security and social spending that were previously possible to defer.

The Taiwan Strait risk alone casts a shadow over every global supply chain that depends on semiconductor production, which is to say virtually every supply chain that matters. Brazil and other Latin American economies are recalibrating their industrial strategies to account for the battery supply chain, which has migrated from the periphery of green-economy planning to the centre of national security doctrine. The Indian Ocean has become a militarised corridor in which maritime insurance costs and the security of strategic ports are directly repricing the cost of global trade.

India sits at the intersection of these pressures. As we noted in March, India is moving beyond headline growth toward structural depth. Part of that depth now involves a substantial expansion in domestic defence production and an accelerating push toward semiconductor self-reliance. The trade-offs are significant and largely underreported. Every rupee committed to a naval carrier programme is a rupee that is not available for rural infrastructure, public health, or the quality of state-level governance. This is not a critique of Indian strategic ambition. It is a recognition of the arithmetic that every government navigating the 2026 fiscal landscape must confront.

This edition of The Meridian does not treat war as spectacle. We treat conflict as a structural case study in political economy, with all the analytical rigour that framing demands. We examine the lobbying ledger that connects defence contractors to political capital, and the diplomacy-arms paradox in which governments advocate publicly for de-escalation while simultaneously accelerating their weapons exports. We investigate the economics of cognitive warfare and the disinformation industries that have emerged to manufacture the popular consent on which these expenditures ultimately depend.

The question this edition asks, and does not pretend to answer definitively, is whether the global systems now bearing the weight of renewed great-power competition are structurally equipped to endure what the coming decade will require of them. Growth alone, as we argued last month, is insufficient to guarantee resilience. The quality of the underlying systems is what matters: the depth of industrial capacity, the reliability of energy infrastructure, the integrity of financial architecture, and the political capacity to make and sustain difficult decisions under conditions of sustained pressure.

War may be decided in wood-panelled rooms and on contested ridgelines. But it is sustained, and ultimately resolved, by the relentless arithmetic of the economy. If you wish to understand where the world is heading in 2026, you must look at the ledger.

Everything else is noise.

April 2026 · War Economy Edition