Money and Supply

Understanding modern conflict requires more than identifying where the fighting occurs. It requires mapping the economic systems that sustain those conflicts: the factories producing ammunition, the shipping lanes carrying energy, the financial networks clearing payments and the resource flows that keep armies operating across years of attrition. As of 2026, the number of active armed conflicts worldwide is the highest recorded since the end of the Cold War. These conflicts vary enormously in scale and intensity, but together they reveal a common and largely underreported pattern. War has become deeply embedded within the architecture of the global economy, and the global economy has, in turn, become a structural enabler of war.

The battlefield represents only the visible layer of a far larger system. A missile fired on a contested front line may contain components manufactured across a dozen countries. A tanker transporting oil through a conflict-adjacent strait may be insured in a jurisdiction with no direct stake in the conflict. Payments for military equipment move through digital settlement platforms that exist entirely outside traditional banking networks. The map of war is therefore no longer drawn only with borders. It is drawn with supply chains, and those supply chains connect every major economy on earth to the violence being conducted in its name, or in spite of it.

The map of war is no longer drawn only with borders. It is drawn with supply chains, and those supply chains connect every major economy on earth to conflicts conducted in its name, or in spite of it.

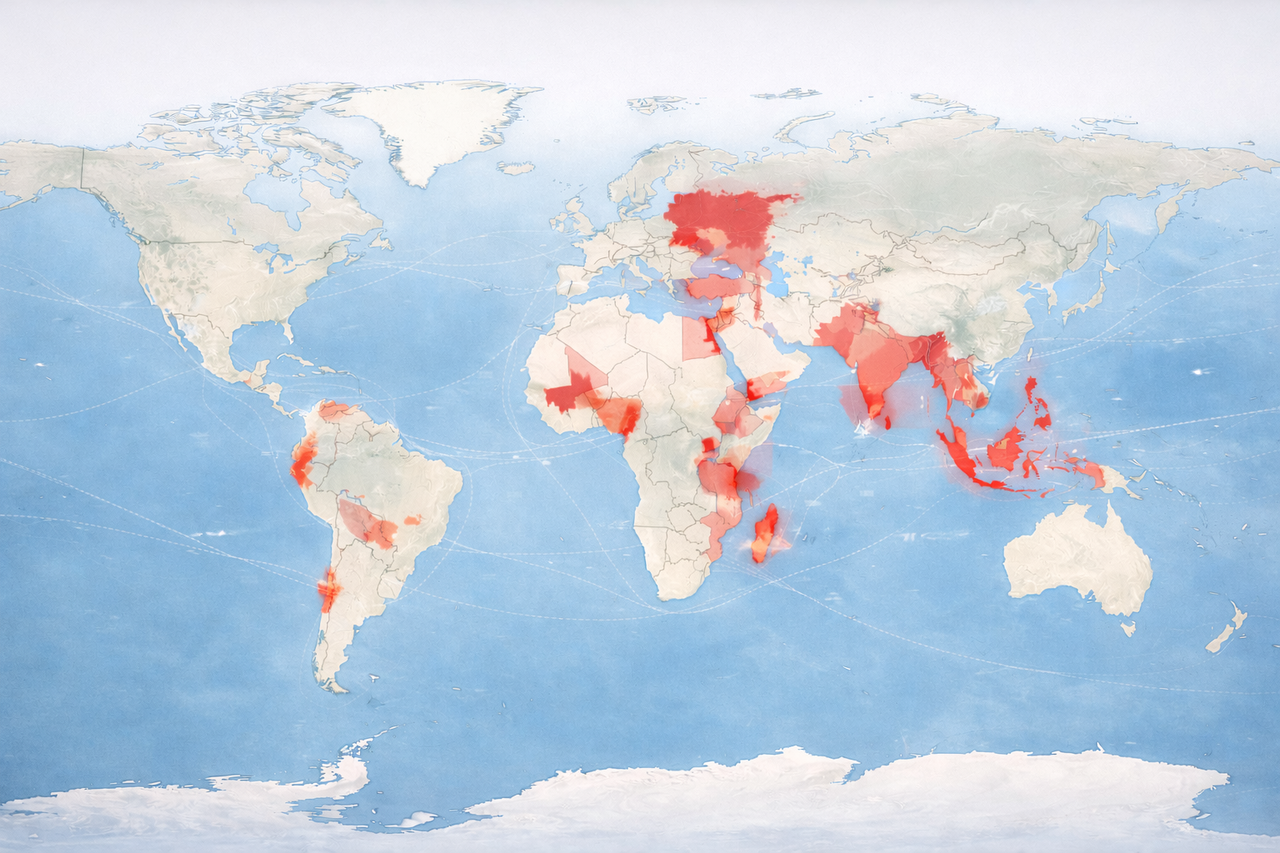

The Meridian · Global Conflict Map · April 2026The war in Ukraine represents the largest conventional conflict currently underway on earth, and it is reshaping the economics of defence production across the entire Western alliance. What began in February 2022 as a rapid invasion has evolved into a prolonged war of attrition defined not by battlefield manoeuvre but by industrial endurance: the capacity to manufacture, transport and deploy artillery shells, drone components, missiles and air defence systems faster than the adversary can consume or destroy them.

Ukraine's military operations depend heavily on Western logistical support of a scale and complexity that has no post-Cold War precedent. NATO countries have dramatically expanded ammunition production and reopened dormant manufacturing lines to sustain the Ukrainian war effort. Factories across Poland, Czechia, Germany and the United States have been converted or expanded specifically to produce 155mm artillery shells, which are consumed in Ukraine at rates that repeatedly outpace production capacity. The economic consequence is a structural repricing of European defence industrial investment that will persist long after the conflict itself concludes.

Russia, meanwhile, has executed a comprehensive wartime economic mobilisation. Defence spending now accounts for an estimated 7.1 per cent of GDP and 19 per cent of all government expenditure, figures that place Russia among the most militarised economies in the world by fiscal share. Industrial facilities across the country have been repurposed for continuous military production, while Moscow has developed procurement networks across North Korea, Iran and Central Asia to obtain critical components that Western sanctions have attempted to deny. The war's central lesson is blunt: victory in a prolonged conventional conflict is determined not by the opening engagement but by industrial endurance, and industrial endurance is a function of economic architecture, not military doctrine.

The Middle East remains one of the most strategically significant conflict regions in the world for a reason that is entirely economic: it controls the arteries through which global energy supply moves. Tensions involving Israel, Gaza and regional actors do not exist in isolation. They intersect with wider geopolitical rivalries and, critically, with the security of maritime corridors whose disruption would transmit economic shock across the entire global system within days.

The Strait of Hormuz alone carries approximately one-fifth of global oil supply. Any sustained disruption to shipping through this 39-kilometre-wide waterway would immediately affect global energy prices, with downstream consequences for inflation, monetary policy and fiscal capacity across every importing economy. The Gaza conflict, which has claimed over 72,123 Palestinian lives according to the Ministry of Health as of March 2026, cannot be understood in isolation from this wider energy security calculus, and the political economies that sustain it.

The maritime dimension has also exposed a structural vulnerability in the global insurance architecture. When Lloyd's of London and other major underwriters designate regions as high-risk, shipping costs rise sharply, forcing traders to seek alternative arrangements. This dynamic has accelerated the growth of shadow shipping networks operating under obscured ownership, alternative insurance pools and irregular tracking signals. The result is the emergence of a parallel energy economy operating alongside official global markets, one that is largely invisible to Western regulators and impervious to the sanctions regimes designed to constrain it.

The so-called dark fleet now numbers an estimated 600 to 700 vessels according to maritime intelligence firm Windward. These ships, many carrying Russian and Iranian oil, operate with falsified documentation, AIS signal manipulation and ownership structures that pass through multiple shell company layers across several jurisdictions. The fleet represents not merely a sanctions circumvention mechanism but a permanent structural feature of the global energy market.

Across West Africa's Sahel region, conflict is driven less by conventional interstate war and more by insurgency, political instability and competition over natural resources, particularly gold. Countries including Mali, Burkina Faso and Niger have experienced repeated military coups over the past five years, and growing insecurity as armed groups including JNIM and Islamic State affiliates expand their territorial influence southward toward the coastal economies of Ghana, Benin and Ivory Coast.

Gold plays a particularly important role in the region's war economy. Control over artisanal gold mines provides armed groups with a steady revenue stream that can be converted into weapons, vehicles and logistical support outside the formal banking system. Unlike digital financial transfers, gold can be transported across borders physically and sold through informal trading networks across West Africa, the Gulf and beyond. This makes it an ideal funding mechanism for armed organisations that operate entirely outside the reach of Western financial sanctions. The Sahel therefore illustrates how resource economies can sustain prolonged instability even in the absence of large-scale state militaries, and why the standard toolkit of financial coercion is structurally inadequate to address it.

In contrast to the active battlefields of Europe or Africa, the Indo-Pacific is defined more by strategic rivalry than by open warfare. But the economic stakes of potential conflict here dwarf those of every other theatre combined. The South China Sea represents one of the most important maritime zones on the planet. Nearly one-third of global trade passes through these waters each year, including the shipping routes connecting East Asian manufacturing centres with Europe, North America and the rest of the world.

Territorial disputes between China and neighbouring states, including the Philippines, Vietnam and Malaysia, have produced a steady militarisation of the region. Naval fleets are expanding rapidly across every major state in the area, and military infrastructure on disputed reef formations continues to grow despite repeated international legal rulings against it. A large-scale conflict has not erupted, but the economic consequences of any disruption to these shipping lanes would be immediate and structural. Global manufacturing supply chains, particularly those involving semiconductor production concentrated in Taiwan, South Korea and Japan, depend entirely on the stability of this maritime corridor. Any disruption to Taiwan Strait shipping alone would trigger a global semiconductor supply crisis within weeks.

Another key node in the global conflict map lies along the Red Sea and the Horn of Africa. This corridor connects Europe and Asia through the Suez Canal and represents one of the most heavily trafficked maritime trade routes in the world, carrying approximately 12 per cent of global merchandise trade in normal conditions. Instability in Yemen, Sudan and Somalia has created persistent and intensifying security risks for commercial shipping across this route.

Houthi attacks on commercial vessels in the Red Sea, which escalated sharply in late 2023 and continued through 2025, have forced major shipping companies to reroute vessels around the Cape of Good Hope. This diversion adds approximately 10 to 14 days to voyages between Asia and Europe and increases fuel costs substantially. The economic ripple effects are not limited to shipping companies. Extended transit times tighten global supply chains, increase inventory costs and push up freight insurance premiums in ways that eventually reach the consumer price level. A geopolitical conflict in Yemen is directly repricing goods in Rotterdam, Hamburg and Felixstowe.

While Latin America is not currently experiencing large-scale interstate wars, several countries are navigating a different form of conflict: hybrid warfare involving criminal organisations of paramilitary scale. Drug trafficking cartels and organised crime networks in Mexico, Colombia, Ecuador and Brazil have developed financial and logistical systems that rival those of state actors in complexity and geographic reach.

These organisations control major trade corridors for narcotics and weapons while operating financial structures that include offshore shell companies, cryptocurrency settlement networks and trade-based money laundering schemes disguised as legitimate import and export activity. The line between organised crime and paramilitary conflict is not merely blurred in these contexts. It has effectively dissolved. The cartel is the state in significant parts of several countries, and the economic infrastructure it controls is indistinguishable from the infrastructure of a shadow government. For the Global South, and for the institutions attempting to build durable governance in these regions, this represents a structural challenge that conventional security responses have consistently failed to address.

Viewed together, these conflicts reveal something structurally important that individual reporting on each theatre tends to obscure. Modern wars are not isolated events. They are embedded within, and sustained by, the same global systems of energy, finance, logistics and technology that constitute the peacetime economy. The factory producing ammunition in Pennsylvania is connected to the front line in Zaporizhzhia. The insurance market in London determines which ships carry oil from Kharg Island. The gold trading network in Dubai links an artisanal mine in Mali to a weapons shipment somewhere in the Sahel. These are not incidental relationships. They are structural ones.

Three economic forces underpin the current global conflict environment and will continue to shape it for the decade ahead. First, competition for strategic resources remains intense and is accelerating. Oil, natural gas, rare earth minerals and critical metals are essential not only for economic growth but for the military technologies that define contemporary deterrence. Second, supply chain security has become a central element of national strategy, with governments across every income level now viewing industrial capacity in semiconductors, shipbuilding and energy infrastructure as existential national security concerns rather than merely commercial priorities. Third, financial systems are adapting to conflict in ways that steadily erode the effectiveness of Western economic coercion. Alternative payment networks, digital currencies and sovereign insurance arrangements are not marginal innovations. They are structural responses to a structural pressure, and they are working.

The global conflict landscape of 2026 therefore presents a world defined not by a single dominant war but by multiple overlapping tensions whose economic infrastructure is deeply and deliberately entangled. Major powers rarely confront each other directly. Instead they compete through proxies, economic pressure and strategic positioning across different regions, while simultaneously maintaining the trade and financial relationships that make direct confrontation too costly to sustain. This produces a durable paradox. The global economy remains interconnected through trade and finance, yet those same networks can be and are being repurposed to sustain conflict, finance insurgency and circumvent the sanctions designed to contain them.

Understanding modern war therefore requires looking beyond the front lines. It requires examining the infrastructure of power: the factories, shipping routes, financial systems and resource networks that ultimately determine how wars are fought, who can sustain them and how long they last. The map of war is no longer drawn only with borders. It is drawn with supply chains. And supply chains, unlike borders, have no fixed position on the map.

The six conflict theatres examined in this analysis are not separate crises to be managed in sequence. They are interconnected nodes in a single global war economy, each drawing on shared industrial, financial and logistical infrastructure. Policymakers who address them individually will consistently find that pressure applied in one theatre migrates to another. The architecture of modern conflict is systemic, and only systemic analysis can adequately account for it.

The map of war is drawn with supply chains. Understanding those chains is the prerequisite for any serious attempt to shorten them.

April 2026 · War Economy Edition