The Numbers Speak: Mauritius's Economic Record From Covid to Today and the Questions No One in Parliament Is Asking

In 2020, median real GDP per capita growth globally was lower than during both World Wars. More than 90 per cent of the world's economies contracted simultaneously — the most geographically widespread shock since 1870. Mauritius contracted 20.98 per cent. It then recovered 28.9 per cent by 2023, restoring near pre-Covid levels. Growth is now decelerating to 2.5 per cent in 2026. Public debt stands at 90 per cent of GDP. The CSG was introduced because someone understood the pension mathematics before the crisis arrived. The Meridian Intelligence Desk places these numbers on the record and asks the questions that the parliamentary narrative, focused on assigning blame for the past, is not asking about the present and the future.

There is a difference between political argument and economic analysis. Political argument selects data to support a predetermined conclusion. Economic analysis assembles all available verified data and asks what it actually shows. The Meridian publishes exclusively in the second register. What the verified economic data of Mauritius from 2019 to 2026 shows is a picture considerably more complex, considerably more global in its causes and considerably more demanding in its implications than any parliamentary speech on either side of the chamber has yet captured. The data does not exonerate anyone. It does not condemn anyone. It describes a small island economy that absorbed the most geographically widespread economic shock since 1870, recovered with reasonable speed, accumulated substantial debt in the process, introduced a structurally sound pension reform that is now being legally challenged, and is now navigating decelerating growth in the context of an Iran war oil premium it cannot control. That is the economic reality. The questions it generates are about the future, not the past. And those are precisely the questions that are not being asked.

Covid 2020 economic shock median GDP per capita World Wars global recession unprecedented Forbes SNB

Before any analysis of Mauritius's economic performance can be conducted honestly, the global context of 2020 must be stated precisely. Professor Kristin J. Forbes of the Massachusetts Institute of Technology, delivering the Eighth Karl Brunner Distinguished Lecture at the Swiss National Bank in October 2024, stated that median real GDP per capita growth in 2020 was lower than during both World Wars. This is not a claim about absolute wealth — the world in 2020 was vastly wealthier in absolute terms than during either war. It is a claim about the distribution of the shock. During both World Wars, devastation was geographically concentrated in belligerent nations while the median country — the one exactly in the middle of the global distribution from worst growth to best — remained relatively stable. In 2020, over 90 per cent of the world's economies contracted simultaneously. The median country suffered a severe contraction because there was almost no country left in the distribution that was not contracting. There was nowhere to hide. No safe haven. No trading partner whose stability could offset another's collapse.

The World Bank confirmed this independently: the 2020 contraction was the deepest global recession since the Second World War, and more than 90 per cent of national economies experienced a contraction in per capita GDP simultaneously — the highest proportion of countries shrinking at the same time since 1870. This global context is not a political argument. It is a verified empirical finding from the World Bank and from a lecture delivered at the central bank of Switzerland by one of the world's leading monetary economists. Any economic analysis of any country's performance in 2020 that does not begin with this context is missing the most important fact about the period it is analysing.

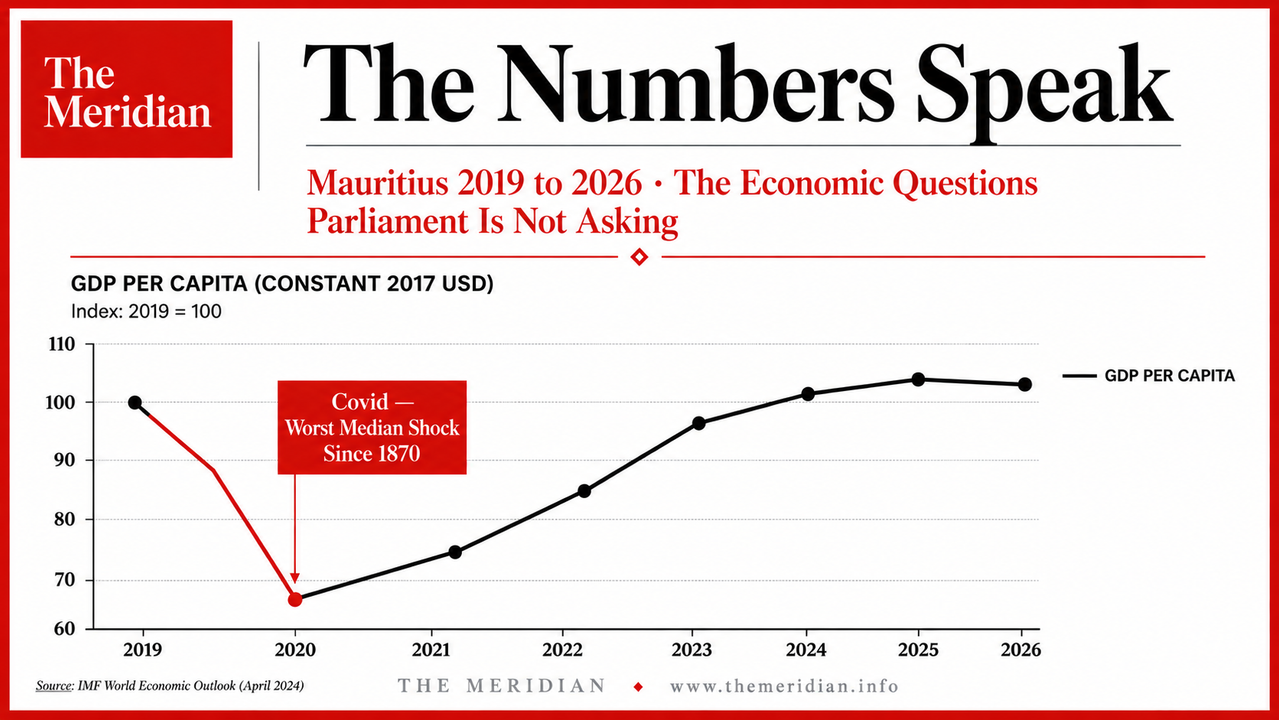

Mauritius GDP per capita 2019 2020 2021 2022 2023 2024 World Bank recovery trajectory

The trajectory above does not tell a story of mismanagement in 2020. It tells the story of a small, open, tourism-dependent island economy absorbing the most severe globally synchronised economic shock since 1870. The 20.98 per cent contraction in GDP per capita in 2020 was not unique to Mauritius. It was the Mauritian expression of a global event that hit every open tourism economy harder than the average because tourism — the sector most directly eliminated by the pandemic — is exactly the sector on which Mauritius depends most heavily. The Maldives, Seychelles, Caribbean island states and Pacific island economies all experienced comparable or more severe contractions for the same structural reason. This is the global context. It belongs in the analysis before any domestic attribution of cause.

The recovery from $9,011 in 2020 to $11,613 in 2023 — a 28.9 per cent increase in three years — is a verified fact. It placed Mauritius at near pre-Covid GDP per capita levels by 2023 despite the global inflationary environment, the rupee depreciation pressure and the fiscal constraints of the period. The World Bank's own country overview for May 2026 notes record tourist arrivals and continued expansion in financial services and ICT as drivers of the 2023-2024 performance. Growth then moderated to 3.2 per cent in 2025 and is projected at approximately 2.5 per cent in 2026, reflecting the completion of major infrastructure projects, a slowdown in new investment and the external headwinds of the Iran war oil premium. These are the numbers. They are what they are.

The 2020 contraction was the most widespread simultaneous economic shock since 1870. No government on earth was designed to withstand it. The question is not who caused it. The question is what is being built now to ensure the next shock — and there will be a next shock — finds Mauritius better prepared than the last one did.

Mauritius CSG Contribution Sociale Generalisee pension reform BRP sustainability IMF

The Contribution Sociale Généralisée deserves specific analytical treatment because it has been among the most politically contested economic policy decisions of recent years, and because the economic argument for it is considerably stronger than the political debate around it has acknowledged. The BRP is non-contributory. It is paid from the Consolidated Fund — general taxation — with no prior contribution from recipients. As the elderly population grows and the working-age tax base shrinks, the cost of funding it from general taxation rises without any corresponding revenue stream specifically designated to meet it. In 2024-25, the BRP cost over Rs55 billion, having more than doubled since 2019. The old-age dependency ratio is projected to double over the next thirty years. The fertility rate is 1.34.

The CSG was introduced to create a contributory revenue stream — a mechanism by which social welfare benefits are partially financed by earnings-related contributions rather than entirely by general taxation. The IMF's Article IV Consultation Report 2025 endorsed the principle explicitly: there is scope for streamlining broadly targeted and regressive fiscal transfers, and an alignment in the BRP eligibility age would help make the pension system more sustainable while containing intergenerational inequalities. The Finance Act 2025, which raises the BRP eligibility age from 60 to 65 over ten years, is the most structurally sound reform Mauritius has enacted in a generation — not because it is popular, but because the alternative is a pension bill that grows faster than the economy can fund it. The Supreme Court challenge to its constitutionality is a legitimate legal process. The economic logic behind the reform is not in question among any serious fiscal analyst.

Mauritius economic questions 2026 debt growth deceleration youth pension reform strategy parliament

The Meridian does not adjudicate political disputes. What it does is identify the economic questions that the available data demands and that the parliamentary record is not addressing. Here are six.

Mauritius economic future debt growth pension water infrastructure Iran war global context 2026

The Iran war oil premium is real and it is not Mauritius's fault. The global deceleration in external demand is real and it is not Mauritius's fault. The demographic pyramid created by a fertility rate of 1.34 and a growing elderly population is real and it was not created by any single government decision in any single electoral cycle. The Rs642 billion public debt accumulated across multiple administrations and multiple electoral cycles. The 30-year-old reservoir plans that remain unbuilt were not unbuilt by one government alone.

The economic situation Mauritius faces in May 2026 is the compound result of structural decisions made across decades, amplified by a global supply shock that the World Bank confirms was the most widespread simultaneous economic crisis since 1870, compounded further by an Iran war oil premium that arrived at the worst possible moment for a small island importing 100 per cent of its petroleum. No parliamentary speech attributing this compound reality to any single period of government captures what the data actually shows. And no parliamentary speech focused on the past is addressing the six questions the data demands be answered about the future.

The numbers speak. They speak about a Covid shock that was historically unprecedented in its geographic breadth. They speak about a recovery that was genuine and substantial. They speak about a debt level that requires a credible reduction plan. They speak about decelerating growth that requires a credible investment pipeline. They speak about pension reform that is economically correct and politically contested. They speak about youth unemployment that coexists with near-peak GDP per capita in a way that cannot continue indefinitely. And they speak about water and energy infrastructure deficits that no amount of parliamentary debate about the past will build. The Meridian has placed the numbers on the record. The questions belong to Mauritius.

Add comment

Comments