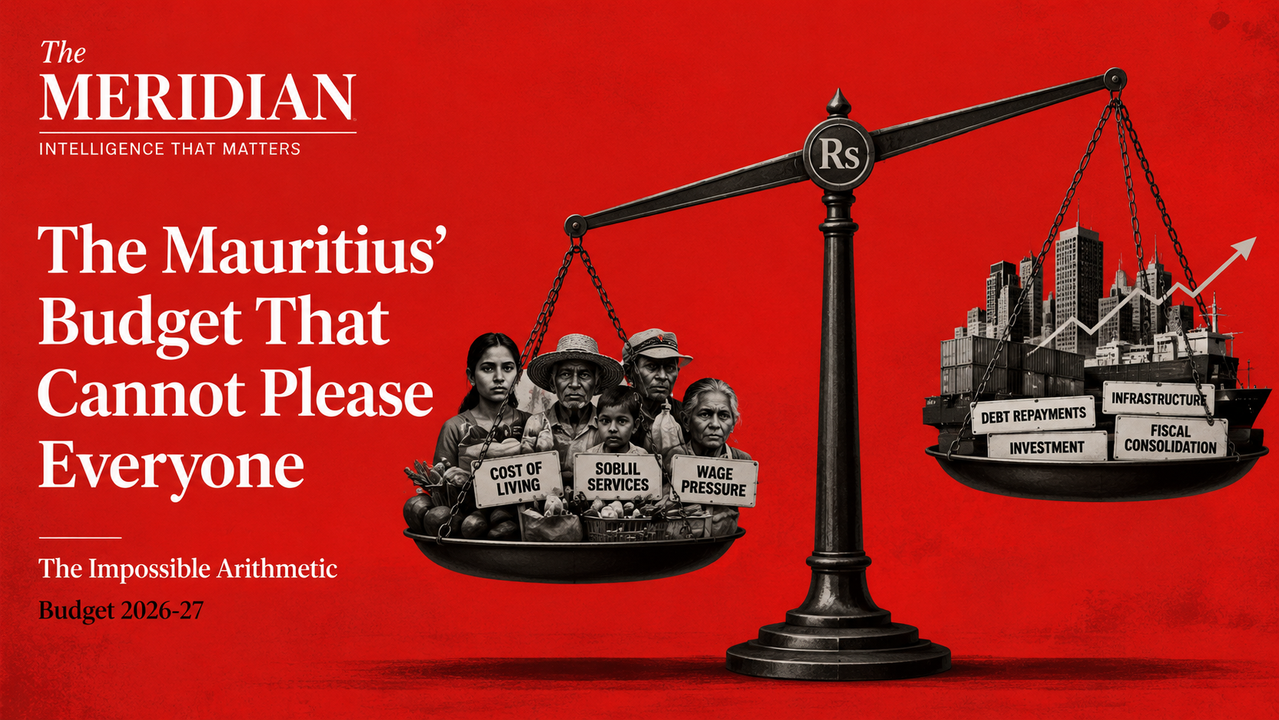

The Budget That Cannot Please Everyone

The Mauritius budget 2026-27 arrives in a fiscal environment with no precedent in the post-independence era. Government debt at 82 per cent of GDP, a structural deficit above 5 per cent, a Moody's negative outlook one notch above junk, and pension spending on a trajectory that the working population cannot sustain. The Ramgoolam government cannot satisfy pension reform, debt consolidation and social spending simultaneously. Something gives. The question is what, and who pays.

Every government inherits the accounts of its predecessor. The Ramgoolam administration, elected in November 2024, inherited something more uncomfortable than the usual fiscal untidiness that accompanies a change of power in Mauritius. It inherited accounts that its own finance minister has described as having been misrepresented, a characterisation now before the courts as the former finance minister and former central bank governor face fraud charges. The Mauritius budget 2026-27, due in the coming weeks, must therefore do two things simultaneously: begin restoring fiscal credibility to a sovereign whose credit rating is under formal negative watch, and maintain the social spending commitments that a population under cost-of-living pressure expects. These two objectives are not easily reconciled. The arithmetic does not permit it.

The headline numbers are familiar by now but bear repeating in full because the political conversation in Mauritius has a tendency to abstract them into percentages and projections that obscure what they mean in practice. Government debt-to-GDP stood at 82.1 per cent at the end of 2024, according to the Bank of Mauritius. The fiscal deficit for 2024 was 5.7 per cent of GDP. The 2025-26 deficit, according to Moody's January 2026 assessment, is estimated at 6.4 per cent of GDP, still substantially above the government's own target of 4.9 per cent. Debt service consumed 43.7 per cent of total government expenditure in fiscal year 2022-23. These are not numbers that stabilise without deliberate action. They are numbers that compound.

Bank of Mauritius

Moody's, January 2026

FY 2022-23

One notch above speculative

The Moody's negative outlook on Mauritius's Baa3 rating is not a warning that can be managed through public relations. It is a formal signal that the agency's analysts believe the probability of a downgrade has increased, and it comes with an explicit statement of what would trigger that downgrade: delays in fiscal consolidation that lead to persistently high deficits, causing debt to at best stabilise at high levels. A downgrade from Baa3 would move Mauritius into speculative-grade territory, a threshold that carries automatic consequences. Institutional investors governed by mandates that prohibit holding sub-investment-grade sovereign debt would be forced sellers of Mauritian government paper. The cost of new borrowing would rise. The financial sector, which positions itself globally as a stable, investment-grade jurisdiction, would face reputational damage at precisely the moment when Morocco's competitive challenge for African financial centre leadership is most acute.

The government's stated fiscal consolidation path targets a deficit of 4.9 per cent of GDP for 2025-26 and a gradual return toward 3 per cent over the medium term. Moody's has acknowledged the direction of travel while questioning whether the pace is adequate. The gap between the government's own target of 4.9 per cent and the agency's estimate of 6.4 per cent for the current fiscal year is not a rounding error. It is a signal that the spending pressures the government faces are larger than its consolidation plan assumed, or that the revenue projections underpinning the plan were optimistic, or both.

A downgrade from Baa3 would strip Mauritius of investment-grade status. The financial sector, already losing ground to Morocco, cannot absorb that signal without structural damage.

The second constraint on the budget is demographic and long-run but it is not distant. Mauritius's population is ageing faster than any comparable small island developing state in the Indian Ocean. The median age is currently 38.3 years and projected to reach 50.1 years by 2050. The share of the population aged 60 and over will reach 30 per cent by the same date. The IMF working paper on Mauritius pension sustainability published in 2015 projected public pension spending rising from 3.7 per cent of GDP in 2013 to exceed 11 per cent by 2060 absent reform. That projection has not improved in the intervening decade. The demographic dynamics driving it have accelerated.

The Basic Retirement Pension, the universal non-contributory pension paid to all Mauritius residents over 60, is the largest single source of this pressure. It is politically the most difficult to reform because it is universal, it is visible in every household and it has been used as a campaign commitment by every political party that has sought power in the last two decades. The Ramgoolam administration, elected on a platform that included social protection commitments, faces the same structural logic that has prevented every previous government from making the pension reform that the IMF, the World Bank and independent economists have repeatedly identified as unavoidable: the political cost of reform is immediate and concentrated, while the fiscal benefit is deferred and diffuse.

The budget for 2026-27 will almost certainly not deliver structural pension reform. What it may deliver is a set of incremental measures, an adjustment to the contribution rate, a modest increase in the retirement age, a tightening of eligibility conditions at the margins, that allows the government to signal reform intent without incurring the full political cost of genuine structural change. Whether Moody's and the international financial community accept that signal as sufficient to avoid a downgrade is the central uncertainty hanging over the budget preparation process.

The third leg of the impossible triangle is social spending. Mauritius has successfully eliminated extreme poverty and reduced relative poverty from 16.5 per cent of the population in 2020 to an estimated 9 per cent by 2025, according to the Bertelsmann Transformation Index 2026. This achievement rests on a social transfer architecture that includes not only the Basic Retirement Pension but also housing support, social aid, food price subsidies channelled through the STC mechanism, and a range of targeted programmes for vulnerable households. All of these are under fiscal pressure simultaneously.

The cost-of-living dimension of this pressure is acute and politically salient. The rupee has depreciated consistently against the dollar, driven by the structural trade deficit that oil and food imports create. The Iran war has pushed global oil prices to levels that the STC cross-subsidy mechanism must absorb or pass through. Every dollar increase in the Brent crude price increases the import bill in rupee terms by a factor that compounds with the exchange rate weakness. The Mauritian household that was already stretched by the inflation of 2022-24 has not recovered its real purchasing power. A budget that is perceived to reduce social protection in this environment will face political resistance that the governing coalition, with its own internal tensions, may not be able to manage.

The government cannot simultaneously reduce the deficit fast enough to satisfy Moody's, protect the social spending floor that its electoral mandate requires, and begin the pension restructuring that the demographic trajectory makes unavoidable. One of these three will be deferred. The historical pattern in Mauritius is that fiscal consolidation and pension reform are deferred while social spending is protected. If that pattern holds in 2026-27, the credit rating consequence becomes more likely, not less.

A budget that merely postpones the hard choices will not, in the current environment, be good enough. The window within which Mauritius can implement fiscal adjustment at a manageable pace, before the demographic pressures compound the fiscal ones and before a potential credit downgrade raises the cost of adjustment, is closing. The 2026-27 budget is not the last opportunity to act, but it is the most important opportunity the Ramgoolam administration will have to demonstrate that it understands the structural nature of the challenge rather than treating it as a short-term cash management problem.

What would a credible budget look like? It would contain a revenue mobilisation component that broadens the tax base beyond the current reliance on consumption taxes and import duties, which are regressive and volatile. It would announce a pension reform process, not merely reform intent, with a legislated timeline and an independent actuarial review. It would publish a medium-term fiscal framework with specific, quantified consolidation targets that go beyond the next twelve months. And it would be honest with the Mauritian public about what the numbers mean, that the island is carrying a debt burden and a demographic trajectory that require sacrifices from everyone, not from the most vulnerable alone.

Whether the government delivers a budget of this quality is a question about political will as much as technical capacity. The Ramgoolam administration has the benefit of having inherited a situation bad enough to justify difficult measures and the political capital of a fresh electoral mandate. It also has the constraint of a coalition that includes partners with their own distributional priorities and a public that has been told for too long that fiscal prudence and social protection are compatible without hard choices. The budget will reveal which of these forces is stronger.

Add comment

Comments