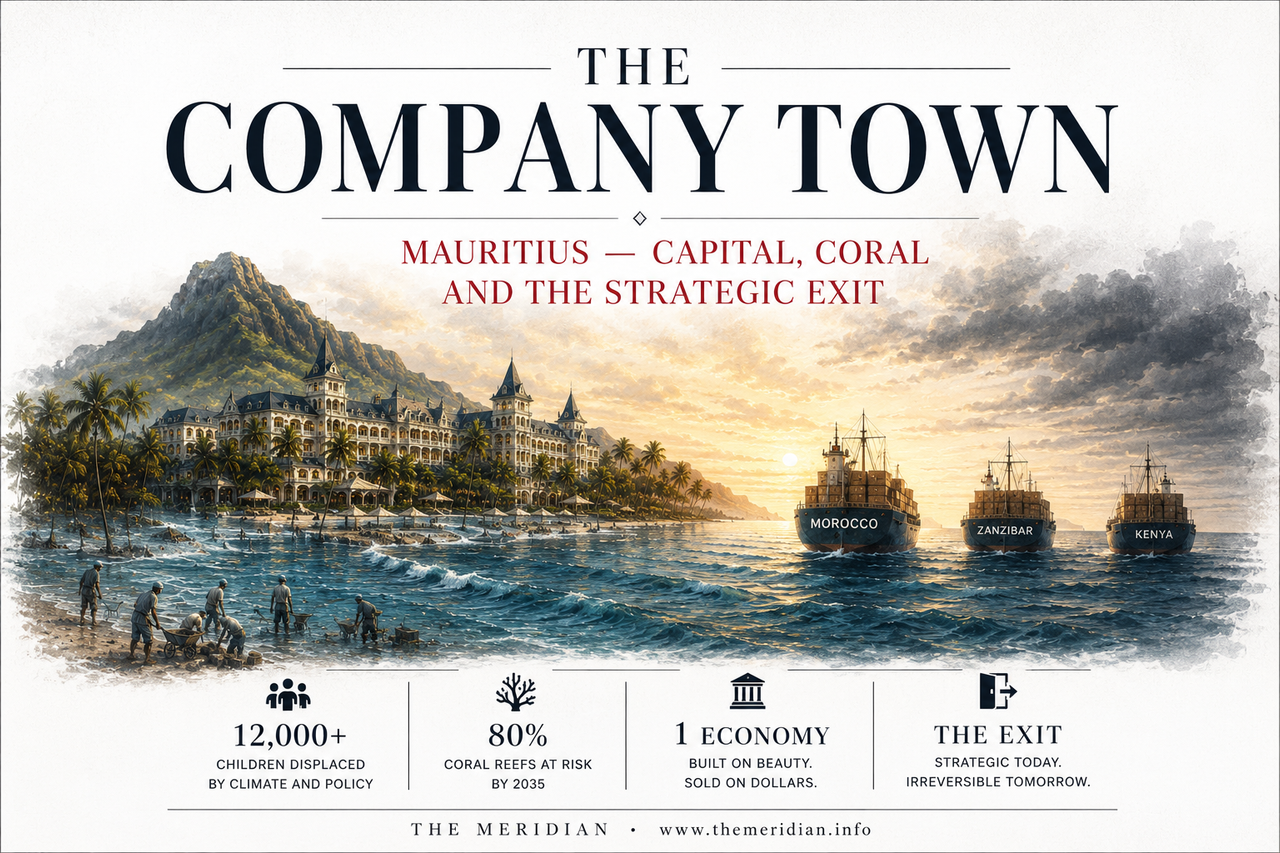

The Company Town: How Mauritius's Conglomerates Are Positioning for an Exit Before the Island Goes Underwater

A company town is a place where one company, or a small group of companies, controls not just the economy but the conditions of life: the jobs, the wages, the housing, the shops, the political conversation. Mauritius has become one at national scale. A handful of conglomerates control tourism, retail, manufacturing, shipping, financial services and real estate. They employ tens of thousands at minimum wage. They import cheap labour to sustain margins. They receive public bailouts when crises hit and deploy the profits of recovery to Morocco, Zanzibar and Kenya. And the coral reefs are bleaching. The beaches are eroding. The sea is rising. The Meridian asks the question no one in Port Louis is asking publicly: do they know something about the island's future that the rest of us do not?

There is a concept in economic history called the company town. It describes a settlement such as a mining town in Appalachia, a plantation in the colonial tropics or a factory district in industrial Lancashire, in which the economic and social life of the community is so completely dominated by a single enterprise or a small group of enterprises that the distinction between the corporation and the state effectively dissolves. The company owns the houses, runs the shops, employs the workforce, funds the hospital and school and church, and sets the terms on which everyone in the community participates in economic life. The company town is not a conspiracy. It is a structural outcome: the result of a small geography, a limited economic base and the concentration of capital that follows when a few actors move faster, invest more aggressively and capture the institutional environment more effectively than anyone else. Mauritius has become a company town. Not through malice. Through structure. And the structure is now producing consequences that the official narrative, comprising the Mauritian Miracle, the Star and Key of the Indian Ocean and the wealthiest economy in Africa, has never been designed to acknowledge.

Up 15.2%. Operations in 20 countries. 40,000 employees

EBITDA margin 28.4%. Expanding to Morocco and Zanzibar

Rs212,940 per year. $2.13 USD per hour

Up 26% from 2023. 95% from 4 countries

Ages 15-24. World Bank ILO modelled estimate

Reef degradation accelerating with each event

Mauritius conglomerate capture economy IBL NMH Rogers ENL Omnicane minimum wage labour market

The capture of the Mauritian economy by a small number of conglomerates was not the result of a single decision or a single era. It accumulated over decades through a combination of historical land ownership, access to political networks, the ability to diversify across sectors as each new economic pillar was developed, and the structural advantage that scale confers in a small economy where the barriers to entry for anyone outside the established groups are prohibitively high. IBL, founded in 1830, predates the Mauritian state by 138 years. NMH/Beachcomber has been shaping Mauritius's tourism product since the 1950s. Rogers, ENL and Omnicane trace their origins to the colonial sugar economy that structured the island's land tenure, labour relations and capital concentration before independence in 1968.

The result of this historical accumulation is an economy in which a handful of groups control the supermarkets where Mauritians buy their food, the hotels where foreign tourists sleep, the ships that carry the imports on which the island depends, the insurance policies that protect Mauritian households, the ground handling operations at the airport, the industrial estates where manufacturing occurs and the real estate developments where the next generation of Mauritians cannot afford to buy. This is not a description of a competitive market. It is a description of a company town at national scale, one in which the concentration of economic power in a few hands has produced the same structural dependency, the same wage suppression and the same institutional capture that characterised the classic company towns of economic history, expressed through the sophisticated instruments of a twenty-first century financial conglomerate rather than the blunt tools of a nineteenth century mine owner.

Mauritius conglomerate extraction minimum wage foreign labour profit repatriation dividend surplus

The extraction model operates through three simultaneous mechanisms that The Meridian has documented in this edition through verified primary source data. The first is the wage floor. The national minimum wage of Rs17,745 per month is the legal floor for all sectors, applied equally to a five-star resort generating 35 per cent EBITDA margins and a small manufacturer operating on 5 per cent margins. The conglomerates that operate in the high-margin sectors benefit from a wage floor calibrated to the survival of the low-margin sectors. The gap between the minimum wage and the value generated per employee in hospitality and retail is not the consequence of market forces. It is the consequence of a political economy in which the groups that benefit most from a low wage floor have the greatest capacity to ensure that the floor stays low.

The second mechanism is imported labour. When educated young Mauritians decline to work in hospitality, construction and manufacturing at current wages, which is what 16.61 per cent youth unemployment combined with persistent employer complaints of labour shortage actually means, the market is sending a signal. The signal is that wages are too low to attract the available local workforce. The conglomerate response, supported by government policy, is to import workers from India, Nepal, Madagascar and Bangladesh who accept the current wage rather than to raise the wage to the level that would attract local workers. Forty-seven thousand six hundred and eighty work permits by October 2025, up 26 per cent in two years. The imported worker does not resolve the structural problem. The imported worker is the mechanism by which the structural problem is permanently deferred, at the cost of the Mauritian youth who remains unemployed or emigrates, and at the benefit of the EBITDA margin that remains intact.

The third mechanism is the deployment of surplus. NMH/Beachcomber generated Rs2.5 billion in profit after tax in nine months and is acquiring a five-star resort in Zanzibar and expanding in Morocco. IBL generated Rs3.5 billion in profit from continuing activities in nine months and operates Kenya's largest supermarket chain with 114 stores, has acquired Seybrew in Seychelles and is pursuing its Beyond Borders strategy across East Africa. The surplus generated from Mauritian consumers, Mauritian land, Mauritian workers and publicly subsidised crisis survival through the Mauritius Investment Corporation is being systematically deployed to create productive capacity outside Mauritius. Capital generated here. Value created there. Mauritius receives the wage bill, the tax contribution and the dividend payout. Morocco, Zanzibar, Kenya and the Seychelles receive the investment, the jobs at the new margin frontier and the growth optionality that comes with being the next territory rather than the mature home market.

The company town does not announce its intentions. It simply makes rational economic decisions, one quarter at a time, until the day that Mauritius looks up and finds that the capital has left, the skills have followed and what remains is the infrastructure of extraction without the engine that once drove it.

Mauritius sea level rise coral bleaching tourism climate risk conglomerate exit strategy beaches

This is the part of the analysis that no boardroom in Port Louis will confirm and no annual report will state. But the data is public, the projections are peer-reviewed and the investment decisions are documented. And when you assemble them into a single framework, they point toward a conclusion that is as uncomfortable as it is analytically coherent.

Mauritius's tourism economy is built on three physical assets: its beaches, its lagoons and its coral reefs. The beaches are eroding. The lagoons are warming. The coral reefs are bleaching. The 2016 coral bleaching event affected approximately 27 per cent of Mauritius's reef system, according to Reef Check Mauritius. The 2020 event compounded the damage. The 2024 event was described by marine biologists monitoring the island's reefs as the most severe on record. The IPCC Sixth Assessment Report projects that 70 to 90 per cent of tropical coral reefs will be severely degraded at 1.5 degrees of global warming above pre-industrial levels, a threshold that the current trajectory of emissions suggests will be crossed in the early 2030s. The snorkelling and diving tourism product that contributes significantly to the premium Mauritius commands over competing destinations in the Indian Ocean is built on an ecosystem that the climate science says will be functionally destroyed within the investment horizon of any serious long-term capital allocation decision.

The sea level rise projection compounds this. Under the IPCC's intermediate scenario, global mean sea level rise of 0.4 to 0.6 metres by 2100 is the most likely outcome, with a tail risk of 1 metre or more. For a low-lying island whose tourism infrastructure is concentrated within 50 to 200 metres of the shoreline, a 0.5 metre sea level rise does not merely threaten individual buildings. It changes the geometry of the beach itself, increases the frequency of storm surge flooding, raises the insurance cost of coastal operations and reduces the residual value of beachfront land as a long-term financial asset. The luxury resort that costs Rs500 million to build today will require Rs50 to Rs100 million per decade in coastal protection and maintenance that did not exist in the original investment case. That is a structural shift in the economics of Mauritian coastal tourism that is already visible in the insurance and reinsurance market, where Lloyd's of London and the major reinsurers have been repricing small island coastal risk since approximately 2018.

Now consider the timing of the conglomerate expansion decisions. NMH began its Moroccan expansion in earnest after 2020. The Zanzibar acquisition is being concluded in 2026. IBL's Beyond Borders strategy into East Africa has been the defining strategic theme of the group for the past three years. Morocco's Atlas Mountains and coastal terrain are not subject to the same sea level and coral bleaching risks as Mauritius. Zanzibar's tourism product, while also coastal, is at an earlier stage of development where the premium pricing that compensates for climate risk has not yet been fully established. Kenya's Naivas supermarket chain is entirely inland, entirely climate-resilient and positioned to benefit from Kenya's growing urban middle class over a 20 to 30 year horizon regardless of what happens to Indian Ocean sea levels.

The Meridian is not asserting that Mauritius's conglomerates are executing a coordinated climate exit strategy. Corporate strategy is rarely that explicit. What The Meridian is asserting is that the people who run these organisations are sophisticated long-term capital allocators who read the same IPCC reports that are publicly available, employ the same risk consultants who advise Lloyd's of London on Indian Ocean coastal exposure, and make capital allocation decisions over 10 to 20 year horizons that reflect their assessment of long-term asset value. And their capital allocation decisions, documented in their own published filings, show a systematic reorientation away from Mauritius and toward markets that are geographically, climatically and demographically better positioned for the next generation of growth. The simplest explanation for a pattern of behaviour is usually the correct one.

They are not announcing a departure. They are executing one, rationally and incrementally, one investment decision at a time. Morocco does not bleach. Zanzibar is not going underwater. Kenya's urban middle class is growing. The arithmetic is not complicated.

Mauritius post-conglomerate economy debt infrastructure youth emigration rupee decline future

The scenario The Meridian is describing is not inevitable. It is the trajectory of current trends if no structural intervention occurs. But the trajectory is coherent and the timeline is measurable. Over the next 10 to 20 years, as the climate risk to Mauritius's coastal tourism infrastructure becomes impossible to ignore in balance sheets and insurance markets, the major hotel groups will face a choice between sustained capital reinvestment in a depreciating asset base or the gradual shift of their strategic centre of gravity to their international operations. The IRS and PDS property sale mechanisms already provide the exit infrastructure: beachfront villas and resort properties can be sold to foreign buyers at international prices, converting the climate-exposed physical asset into portable capital that follows the group's international expansion.

The Mauritius that would be left behind in this scenario is one that The Meridian has been documenting throughout this edition. A water system that loses 50 per cent of supply to leaks because the infrastructure was never built despite Rs2.3 to Rs2.5 billion in foreign aid received over a decade. A rupee that has already lost 23 per cent against the dollar over ten years and will lose more as the foreign exchange earnings that tourism provides diminish. A government domestic debt approaching Rs500 billion that was accumulated without building the productive capacity that would allow it to be serviced from domestic growth rather than from further borrowing. A generation of young Mauritians who grew up in a company town that had no offer for them, offering no wages that reflected their education, no housing they could afford and no political voice that changed anything, and who voted with their passports for somewhere else.

The Price Stabilisation Account is in Rs3.2 billion deficit because Mauritius has no strategic petroleum reserve and no renewable energy base sufficient to reduce its oil dependency. The Mare-aux-Vacoas reservoir is at 51 per cent capacity because the reservoir construction plans of 30 years ago were never executed. The mental health system is overwhelmed because it was never funded to the level that a population under sustained economic and now geopolitical pressure requires. These are not the failures of a government that ran out of money. They are the failures of a political economy in which the entities with the greatest capacity to fund public goods through taxation and wage-driven domestic consumption had the greatest structural incentive to prevent the policies that would have required them to do so.

Mauritius economic reform conglomerate accountability climate adaptation wage policy sovereign wealth

The Meridian does not publish this analysis as a counsel of despair. It publishes it as the most honest possible account of where the structural trends are pointing, because an honest account of the problem is the necessary precondition for any serious attempt to resolve it. There is still time. The coral reefs are degraded but not dead. The beaches are eroding but not gone. The young people are leaving but have not all left. The capital is reorienting but has not fully departed. The window is narrow and it is closing, but it exists.

What must change is the political economy of allocation. A sovereign wealth fund, capitalised from a levy on conglomerate profits generated from Mauritian resources and publicly subsidised survival, would create a vehicle for retaining a portion of the surplus that is currently leaving the island with each Morocco acquisition and each Zanzibar resort deal. A climate adaptation fund, modelled on those established by Barbados and the Maldives, would begin the infrastructure investment required to make Mauritius's coastal assets defensible against the sea level rise that the physics of the atmosphere has already made inevitable. A sector-specific minimum wage in hospitality calibrated to the EBITDA margins the sector actually generates would begin the rebalancing of the wage-profit relationship that the imported labour mechanism has deferred for two decades.

None of these interventions requires the dismantling of the conglomerate model. The conglomerates are capable, well-managed organisations that have created genuine value and genuine employment in Mauritius over many decades. What they require is a political economy that reflects the fact that the value they have created was generated not only by the genius of their management but also by the land they hold, the workers who serve at the minimum wage, the public bailouts that kept them alive through crises and the natural assets, namely the reefs, the beaches and the lagoon, that their marketing sells to the world but which belong to no shareholder and which are being destroyed at a rate that no dividend policy accounts for.

The company town has a well-documented historical ending. The mine closes, or the ore runs out, or the factory moves to cheaper labour. The company departs. The town remains. The people who built their lives around the company's promise find themselves in a landscape that has been shaped entirely around an economic model that no longer exists. Mauritius is not there yet. But the ships are being loaded for Morocco and Zanzibar. The coral is bleaching. The young people are at the airport. And the question that every Mauritian, every shareholder, every minimum wage worker and every young graduate looking at a flight to London or Melbourne, deserves an honest answer to is this: when you look at the investment decisions being made today by the institutions that have defined this island's economy for generations, what do they tell you about what those institutions believe about the island's future?

Add comment

Comments