The LNG Race: Who Gets Europe's Contracts and What Happens When Hydrogen Arrives

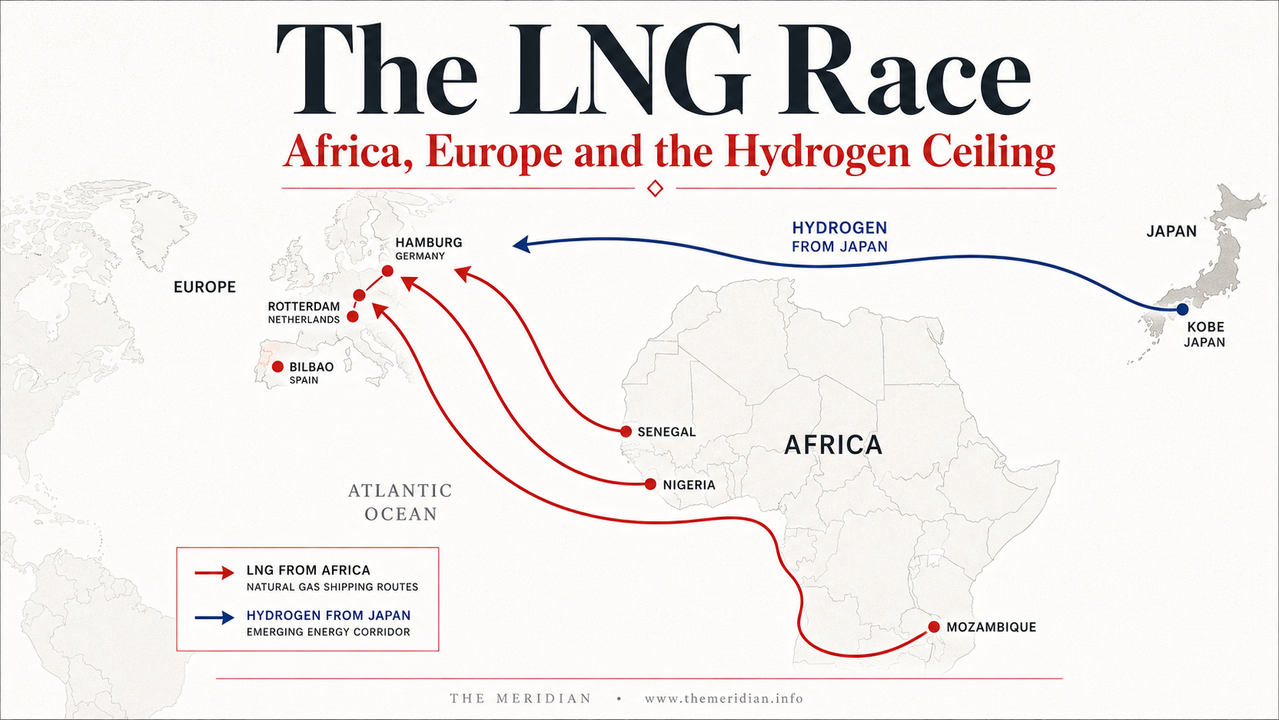

Europe lost approximately 16 million tonnes of Qatari LNG when the Strait of Hormuz closed in February 2026. The European Council simultaneously banned all Russian LNG from March 2026. African producers in Nigeria, Mozambique, Senegal and the Republic of Congo avoid both Hormuz and the Red Sea. The race for European long-term contracts is the most consequential commercial competition in global energy markets right now. But on 11 May 2026, MB Energy, Daimler Truck and Kawasaki Heavy Industries signed a Joint Development Agreement for a liquefied hydrogen supply chain to Hamburg targeting commercial operation in the early 2030s. African LNG producers are competing for a market that has a structural ceiling. The Meridian Intelligence Desk analyses who wins the race and how long the prize lasts.

The Strait of Hormuz has been closed since 28 February 2026. The closure removed Qatar from the European LNG supply equation at a stroke. Qatar had been supplying approximately 16 million tonnes per year to European import terminals, accounting for roughly 16 per cent of total European LNG imports. The loss arrived simultaneously with the European Council's January 2026 regulation prohibiting all Russian LNG imports from 18 March 2026, with a full pipeline gas ban by end-2027. Europe went from managing a gradual diversification away from Russian gas to managing an emergency supply gap in the same quarter. The gap is large, the alternatives are limited and the countries best positioned to fill it are in Africa. Nigeria, Mozambique, Senegal, Algeria and the Republic of Congo are watching European energy ministries and utility procurement teams with a combination of urgency and structural caution. The urgency is real. The structural caution is justified. The race for European contracts is not simply a question of who has the gas. It is a question of who can deliver it, at what breakeven cost and against a demand horizon that the hydrogen transition is beginning to define from above.

Hormuz closure Feb 2026. Approx 16% of EU LNG imports

Full pipeline gas ban end-2027. EU Council Jan 2026

Below historical norms. Summer restocking urgent

Mozambique, Nigeria, Senegal, Tanzania. Africa Oil Gas Report

African LNG Hormuz Red Sea bypass Europe strategic advantage Nigeria Senegal Mozambique Congo 2026

The geopolitical logic favouring African LNG in the current moment is straightforward. LNG exports from Nigeria, Senegal, Mauritania, Gabon and the Republic of Congo avoid both the Strait of Hormuz and the Red Sea, reducing shipping risk, shortening sailing times to European terminals and removing two of the most exposed chokepoints in global gas trade. This advantage predates the current disruption. What has changed is how buyers view it. Before 2026, Atlantic supply was one option among many. Following the loss of Qatari deliveries, which had accounted for roughly 16 million tonnes per year of European supply, diversification away from those routes has become a lasting procurement objective.

The geographic premium that African LNG now commands in European procurement discussions is real and measurable. Before the Hormuz closure, European utilities factored insurance costs and geopolitical risk into procurement decisions as secondary considerations relative to price. After the closure, supply route security has become a primary criterion. A cargo that arrives reliably from the Republic of Congo or Nigeria is worth more to a European utility than a theoretically cheaper cargo from a supplier whose route passes through a contested strait. African LNG producers are expected to emphasise geographic positioning and supply reliability during procurement discussions, with cargo shipments from West and Central Africa avoiding several major maritime chokepoints and reaching European import terminals within relatively short sailing windows.

Nigeria Mozambique Senegal Algeria Congo LNG Europe contracts 2026 producer comparison

Nigeria LNG Train 7 Europe contracts Portugal Spain Iberian terminals 20-year supply agreements 2026

Nigeria remains Africa's LNG backbone, with its volumes historically flowing into Europe's Mediterranean and Atlantic terminals through a mix of long-term contracts and spot cargo transactions. As Russian pipeline volumes have declined, Nigerian LNG has become a significant component of LNG deliveries into Iberian terminals, with Portugal sourcing over half of its LNG from Nigeria and Spain among the key European destinations for Nigerian cargoes. This established market position gives Nigeria a structural advantage in the current race that no other African producer can match. The buyer relationships, the terminal infrastructure, the shipping routes and the regulatory familiarity are all in place.

Nigeria LNG signed a series of 20-year gas supply agreements, securing feedstock of approximately 1.29 billion standard cubic feet per day from the Nigerian National Petroleum Company and key upstream partners. These contracts underpin the company's forthcoming Train 7 expansion at Bonny Island, which will increase liquefaction capacity by nearly a third. For NLNG, long-term agreements provide predictable revenue, while for European buyers, they offer certainty of supply. Nigeria's structural weakness remains its chronic production shortfall relative to quota, driven by pipeline vandalism, theft and infrastructure underinvestment. If Train 7 is commissioned on schedule, Nigeria's LNG position strengthens considerably. If the production problems that have dogged its oil sector extend to gas feedstock, the European window narrows.

Mozambique LNG TotalEnergies restart 2026 Coral FLNG Rovuma ExxonMobil Europe supply Cabo Delgado

Mozambique represents the highest-upside and highest-risk position in the African LNG race. The TotalEnergies-operated Mozambique LNG project, which carries nameplate capacity of 13 million metric tons per year, was relaunched in January 2026 after a five-year suspension. At full capacity, 13 million tonnes per year from a single project would be a transformative addition to European supply, comparable in scale to the Qatari volumes lost to the Hormuz closure. The Coral Sur FLNG had shipped its 100th cargo by April 2025, with the African Development Bank's senior loan for the Coral Norte follow-on reflecting lender confidence in the project's commercial viability.

The pattern is familiar. Mozambique LNG was suspended for more than four years following security disruptions in Cabo Delgado. Large onshore LNG projects concentrate technical, political, security and commercial risk into a single decision point. They then require a wide group of stakeholders, each with different risk tolerances, to commit simultaneously. When one participant hesitates, progress stalls. The gas itself is rarely the constraint. The way risk is packaged and presented to capital is. The Rovuma LNG project led by ExxonMobil is targeting a Final Investment Decision in 2026, aiming for 18 million tonnes per year. If both projects reach full production, the Rovuma Basin alone would add more LNG capacity than Qatar's entire Hormuz-disrupted European export volume. The question is whether the security situation in Cabo Delgado holds through the construction and commissioning cycle.

hydrogen ceiling LNG demand Europe 2030 MB Energy Daimler Kawasaki Hamburg JDA African LNG competition

On 11 May 2026, four days ago, MB Energy, Daimler Truck AG and Kawasaki Heavy Industries signed a Joint Development Agreement at the Hamburg Port Anniversary festival. The three companies will use their respective expertise and proceed with specific studies to establish an economically viable liquefied hydrogen supply chain to the port of Hamburg. The objective is to achieve Commercial Operation Date for the supply of liquefied hydrogen and hydrogen by the early 2030s. Kawasaki Heavy Industries will provide its expertise in the design and manufacture of essential infrastructure, including hydrogen liquefiers, liquid hydrogen storage tanks and LH2 carrier ships. Daimler Truck aims to bring 100 liquid hydrogen powered fuel cell trucks into customer operations from the end of 2026 onwards, with series production for hydrogen powered fuel cell trucks targeted for the early 2030s.

This agreement is not a threat to African LNG in the immediate term. The early 2030s commercial operation date for liquefied hydrogen from Japan to Hamburg is a decade away. But the agreement is strategically significant for African LNG producers for a reason the producer scorecard does not capture: it defines the ceiling above which European LNG demand will not grow, and may begin to decline. By 2027 to 2030, long-term EU contracts for LNG would surpass projected demand. As a result, the EU's exposure to spot LNG would be minimal. The EU is expected to be over-contracted by 30 to 40 billion cubic metres during this period, with the surplus likely being redirected to global LNG markets. If LNG supply outpaces demand, there will be increasing competition between producers. In our assessment, African producers are more vulnerable to price competition than other global producers because they have higher breakeven prices for LNG exports.

The window in which African producers can secure new long-term European contracts on favourable terms is therefore the current period of supply emergency, before the contract book refills and before the hydrogen supply chain begins to compete structurally with LNG for the decarbonisation mandate. African producers are racing to sign contracts during a supply emergency that has opened a window they may never see again. The hydrogen corridor being built from Japan to Hamburg is defining how long that window stays open. The answer is approximately a decade.

African LNG producers are running the race of their lives toward a finishing line that the hydrogen transition is moving. The window is real. The urgency is real. But the prize is transitional, not permanent. How Africa negotiates that transition will determine whether its gas reserves become the foundation for lasting development or a depleted asset at the end of a market that moved on.

Africa LNG strategy domestic obligation long-term contracts Europe hydrogen transition 2026 2030

Buyers are moving beyond spot purchases to contracts that provide predictability, recognising that even as new global supply is expected to come online, volatility and geopolitical risks remain. Nigeria's 20-year feedstock agreements and the NLNG Train 7 expansion are exactly the right instrument for this moment. Long-term contracts provide the revenue predictability that justifies upstream investment, infrastructure development and the political commitment required to sustain production over the period when hydrogen will begin to compete.

The model that Africa's gas producers must resist is the one in which European companies extract maximum value from African gas resources on short-term spot contracts during the supply emergency, then decline long-term offtake agreements as the hydrogen supply chain develops, leaving African countries with stranded upstream investment and declining revenues at the moment when the energy transition requires them to fund domestic power, industrial development and climate adaptation. Africa holds an estimated 620 trillion cubic feet of proven gas reserves. Africa has a rare opportunity in 2026: to leverage geopolitics not just for capital inflows, but for a future where energy abundance translates into broad-based prosperity at home.

The Greater Tortue Ahmeyim model is instructive. The GTA project earmarks 35 million standard cubic feet per day of its output for domestic use in each country, supporting power generation and industrial development alongside exports to global markets. Rather than viewing exports and domestic consumption as competing priorities, this framework links them directly: as production and exports grow, so too does gas availability for local markets. This is the template that Nigeria, Mozambique and the Republic of Congo should embed in their European contract negotiations: domestic market obligations that ensure gas development creates lasting productive capacity at home rather than merely a revenue stream that flows to shareholders while the hydrogen transition renders the upstream investment obsolete.

The LNG race that African producers are running in 2026 is winnable. The supply gap is real. The geographic advantage is real. The European procurement urgency is real. Nigeria can secure its position as the durable Iberian supplier. Mozambique can position its enormous Rovuma reserves as the long-term East African anchor for a diversified European portfolio. Senegal can build on Greater Tortue Ahmeyim's successful first cargoes to establish West Africa as a reliable new supply hub. The Republic of Congo can convert its operational FLNG track record into extended offtake agreements that outlast the current emergency. But the race must be run with full awareness that the finish line is not simply a signed contract. It is a signed contract with domestic development obligations embedded, secured before the hydrogen corridor from Hamburg to Japan makes African LNG a transitional rather than a permanent fixture in Europe's energy architecture.

Add comment

Comments