The Meridian Responds to Forum Sitwayin: The Money Printing Argument That the Governor of the Bank of Mauritius Already Demolished

On 20 May 2026, an opinion piece published on the Facebook group Forum Sitwayin, attributed to Le Philonomiste, made three claims about money printing in Mauritius. The Meridian examined each claim against the verified global record, the official communications of the Bank of Mauritius and the statements of its Governor. We found one technically correct distinction, one claim officially labelled fake news by the central bank itself and one narrative about the cause of current inflation that the Governor of the Bank of Mauritius contradicted publicly before the ink was dry. The Meridian reports what the evidence actually shows.

The Meridian does not engage in partisan debate. It engages with evidence. When a published opinion piece makes factual claims about monetary policy, those claims can be examined against primary sources — the statements of the institution whose actions are being discussed, the data published by that institution and the verified global record of comparable institutional decisions. The Forum Sitwayin opinion piece published on 20 May 2026 made three specific claims about money printing in Mauritius. The Meridian examined all three. The results are below.

Facebook link: https://www.facebook.com/share/p/1Hgh7babC4/

money printing 2020 Fed ECB Bank of England IMF SDR global central banks pandemic response Mauritius

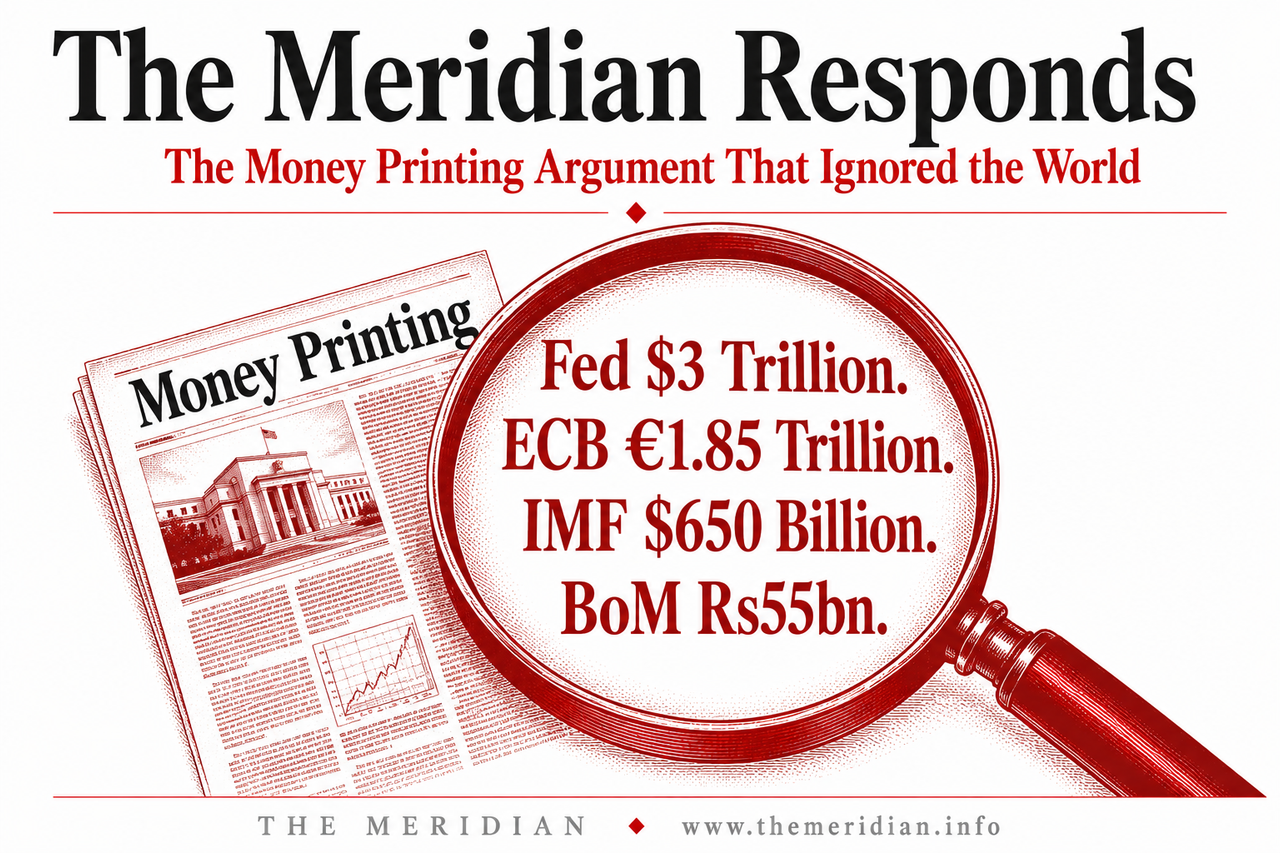

From $4.2tn to $7.4tn. March to December 2020

Launched March 2020. Extended multiple times

Total QE programme expanded to £895bn by end 2020

Largest SDR allocation in IMF history. August 2021

The opinion piece did not mention any of these figures. It examined Mauritius's monetary response to the most severe globally synchronised economic shock since 1870 without reference to what every other major central bank on earth did simultaneously, at a scale that dwarfs Mauritius's response by orders of magnitude. The Federal Reserve alone created more money in 2020 than Mauritius's entire annual GDP multiplied by more than 200 times. This is not a defence of any specific decision. It is the context without which the analysis is incomplete.

Bank of Mauritius FX intervention rupee commercial bank credit expansion import dependency monetary consequences

The opinion piece correctly identifies the technical distinction between central bank base money creation and commercial bank credit expansion. This distinction is real and important in monetary economics. But the opinion piece does not ask the question that the distinction immediately raises in the specific context of Mauritius's structural economy.

If the Rs83 billion in commercial bank credit expansion is non-inflationary and benign — as the opinion piece implies by contrasting it favourably with central bank base money creation — then why has the Bank of Mauritius intervened repeatedly in the foreign exchange market to sell foreign currency and defend the rupee? Mauritius imports 100 per cent of its petroleum, the vast majority of its food and most of its manufactured goods. It does not have a manufacturing export base that generates foreign exchange earnings sufficient to back commercial bank credit expansion. When commercial banks create Rs83 billion in new credit in an economy structured around importing rather than exporting, the demand for foreign exchange rises. The rupee comes under pressure. The central bank must sell reserves to manage that pressure.

The inflationary and exchange rate consequences of credit expansion in a 100 per cent import-dependent economy are real regardless of which institution created the money. The technically correct distinction between base money and broad money does not eliminate this structural reality. It describes a different mechanism producing the same pressure on the external accounts of a small island economy that earns its foreign exchange primarily from tourism and financial services.

Bank of Mauritius rate hike 4.75% inflation imported supply shock Iran war rupee defence middle class

On 20 May 2026, the Monetary Policy Committee of the Bank of Mauritius raised the key rate from 4.50 per cent to 4.75 per cent — the first rate increase in more than a year. The official MPC statement attributed the decision to imported inflation driven by higher energy prices and elevated freight costs from the Iran war, upside risks to the inflation outlook and the need to anchor medium-term inflation expectations. Inflation is expected to average around 5.5 per cent in 2026 under the baseline scenario.

This rate hike is being applied to a supply-side inflationary shock caused by the Hormuz closure and Iran war oil premium. As The Meridian documented in its earlier analysis this month, interest rate increases are a demand-side instrument. They reduce borrowing, slow spending and cool demand. They cannot reopen the Strait of Hormuz. They cannot reduce the war premium on Brent crude above $110 per barrel. They cannot rebuild Suez Canal transit revenues that fell 61 per cent between 2023 and 2024. What the rate hike does in this specific context is make borrowing more expensive for every Mauritian household with a variable rate mortgage, every small business with a commercial loan and every entrepreneur with financing tied to the BoM key rate — while the supply-side inflation that motivated the hike continues to be driven by factors entirely outside any Mauritian institution's control.

The Governor of the Bank of Mauritius told Bloomberg that inflation is caused by the Iran war. The MPC confirmed it is imported and external. The rate hike is the instrument deployed. The middle class is paying the bill for a supply shock it did not cause, managed by a tool that cannot fix it, while a public debate blames a minister for decisions made in 2020 during the worst global shock since 1870.

Mauritius debt reduction plan growth pipeline youth unemployment pension reform water infrastructure questions 2026

The monetary debate currently occupying Mauritius's public commentary — who printed what in 2020, what counts as money printing, what the Rs83 billion figure represents — is a debate about the past. It is a debate about definitions. It is, in the analytical framework The Meridian has applied throughout this edition, a municipal debate: short-term, backward-looking, organised around political attribution rather than structural analysis.

The Meridian published the verified economic data for Mauritius from 2019 to 2026 in The Numbers Speak article earlier this month. That article identified six questions that the parliamentary narrative and the public commentary are not addressing. They have not been answered by the Forum Sitwayin opinion piece. They have not been answered by the parliamentary debate about 2020. They have not been answered by the MPC statement of 20 May. They are the questions that will determine Mauritius's economic trajectory through the next decade regardless of which party is in power and regardless of what monetary decisions were made in 2020.

What is the published strategy for reducing public debt from 90 per cent of GDP to a sustainable level, and over what timeline? What structural investment will reverse the growth deceleration from 3.2 per cent in 2025 to 2.5 per cent in 2026? What specific labour market reforms will reduce youth unemployment from 16.61 per cent in an economy where GDP per capita is near its all-time peak? If the Finance Act 2025 pension reform is overturned by the Supreme Court, what is the alternative fiscal strategy for containing the Rs55 billion per year BRP bill? What is the published plan for building a strategic petroleum reserve before the next oil shock? What is the water infrastructure investment timeline and its funding mechanism?

These are the questions The Meridian is asking. They do not have a political colour. They have a fiscal arithmetic. And the fiscal arithmetic does not care whether the money was printed in 2020 or created by commercial banks in 2025. It cares about the debt trajectory, the growth rate, the investment pipeline and the institutional capacity to deliver what has been promised. The debate Mauritius is having is not the debate Mauritius needs. The Meridian has placed the data on the record. The questions belong to everyone.

Add comment

Comments