The Middle Class Bill: How the 4.75% Rate Hike Defends the Rupee, Triggers a Debt Spiral and Leaves the Poor Paying for a War They Did Not Start

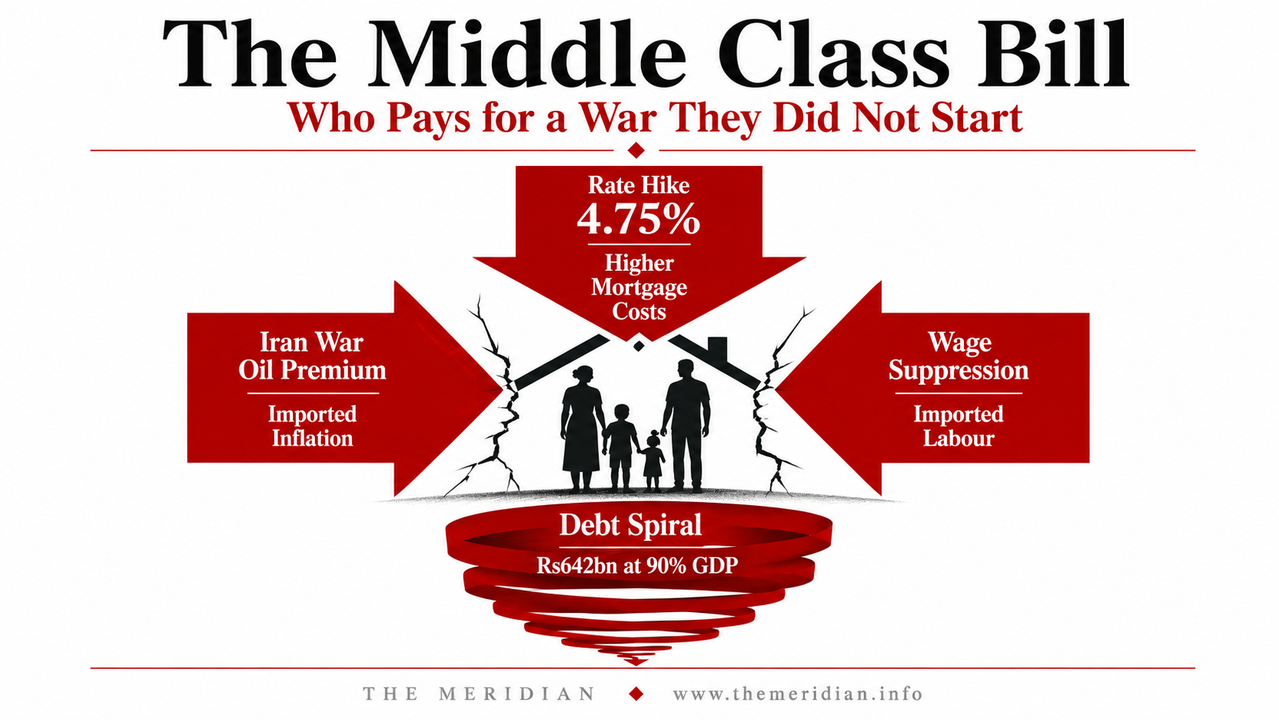

On 20 May 2026, the Monetary Policy Committee of the Bank of Mauritius raised the key rate from 4.50 per cent to 4.75 per cent — the first rate increase in more than a year. Governor Dr Priscilla Muthoora Thakoor told Bloomberg before the meeting that inflation may hit 5 per cent because of the Iran war raising the cost of imported goods. The MPC statement confirmed that imported inflation, driven by higher energy prices and freight costs, is the primary pressure. The tool deployed is a demand-side instrument. The problem is supply-side. The Mauritian middle class will pay the difference. The Meridian analyses the full chain: who the rate hike actually protects, who it actually punishes and what it cannot fix regardless of how many times it is applied.

A rate hike is not a neutral technical event. It is a redistribution. When a central bank raises the cost of borrowing, it transfers income from debtors to creditors, from borrowers to savers, from households with variable rate mortgages to institutions holding fixed income assets. In a country with an equitable distribution of financial assets and liabilities, this redistribution may be broadly balanced across the population. In a country like Mauritius, where the wealthiest households hold inflation-hedging assets including property, equity and foreign currency accounts, while the middle class holds variable rate mortgages and consumer debt, and the poorest households hold nothing at all except their wages, the redistribution is deeply inequitable. The rate hike of 20 May 2026 is not being applied to a neutral economy. It is being applied to a specific Mauritian economy with a specific debt structure, a specific import dependency and a specific social architecture. The Meridian maps exactly who pays.

Up from 4.50%. First increase in over a year. MPC statement

Up from 3.6% forecast in February. BoM MPC May 2026

Higher key rate raises servicing cost on domestic debt

Decelerating from 3.2% in 2025. World Bank May 2026

Bank of Mauritius rate hike rupee defence Iran war imported inflation exchange rate pressure 2026

The official language of the MPC statement is carefully constructed. It speaks of upside risks to the inflation outlook, the need to anchor medium-term inflation expectations and the re-emergence of external pressures. Governor Thakoor told Bloomberg before the meeting that inflation may breach the upper limit of the 2 to 5 per cent target range because of the prolonged Middle East conflict raising the cost of imported goods, specifically fuel and freight. The MPC confirmed that imported inflation, driven by higher energy prices and elevated freight and logistics costs, is the primary pressure.

The Meridian states the mechanism directly. The rate hike is primarily a rupee defence instrument. When the Bank of Mauritius holds rates below the US Federal Reserve's rate, the interest rate differential makes rupee-denominated assets less attractive relative to dollar assets. Capital flows toward dollars. Demand for rupees falls. The rupee depreciates. A depreciating rupee makes every import more expensive in rupee terms — and Mauritius imports 100 per cent of its petroleum, most of its food and all its manufactured goods. Import cost inflation accelerates. The rate hike narrows the interest rate differential, makes rupee assets marginally more attractive and slows the depreciation pressure. This is not inflation targeting in the textbook sense. It is exchange rate management dressed in inflation-targeting language. The official statement is accurate. The mechanism it describes is rupee defence.

The fundamental problem with using a rate hike to defend the rupee against a supply shock caused by the Iran war is that it addresses the symptom without touching the cause. The rupee is under pressure because Mauritius imports in dollars everything that the Iran war has made more expensive. Making rupee borrowing more expensive does not reduce oil prices. It does not reopen the Strait of Hormuz. It does not rebuild Suez Canal revenues that fell 61 per cent between 2023 and 2024. It does not change the structural fact that Mauritius has no strategic petroleum reserve, no domestic energy production and no alternative supply chain for the commodities whose prices are driving the inflation the rate hike claims to fight.

Mauritius rate hike debt spiral credit rating Moody's growth deceleration fiscal deficit borrowing costs 2026

Mauritius middle class mortgage rate hike impact poor household consumption wage suppression imported labour

The rate hike is not experienced equally across Mauritius's social structure. Its impact is determined entirely by a household's balance sheet, specifically what it owes relative to what it owns.

The wealthiest Mauritians hold assets that hedge inflation and are largely unaffected by a rate hike. Property values typically rise with inflation. Equity holdings in conglomerates like IBL and NMH generate dividend income that adjusts with the nominal economy. Foreign currency accounts appreciate when the rupee depreciates. The same rupee weakness that motivates the rate hike actually enriches dollar-denominated asset holders. For this group, the rate hike is a technical monetary event with minimal personal impact.

The middle class Mauritian with a Rs3 million home loan at a variable rate linked to the key rate faces an immediate and concrete monthly cost increase. At a 25 basis point increase on a Rs3 million loan over 20 years, the monthly repayment rises by approximately Rs400 to Rs600 depending on the loan structure. This is not an abstraction. It is Rs400 to Rs600 less available for food, school fees, fuel and the other costs that the Iran war oil premium has simultaneously made more expensive. The middle class household is being squeezed simultaneously by higher mortgage costs from the rate hike, higher fuel costs from the oil premium, higher electricity costs from the CEB tariff increase and stagnant wages suppressed by the imported labour mechanism documented throughout this edition.

The small business owner who borrowed Rs5 million to survive Covid, to invest in equipment, to open a restaurant or a retail outlet, faces higher interest costs on commercial loans that are already stretched by the economic deceleration. Mauritius's small and medium enterprise sector, the primary employer of the middle class and the primary generator of economic mobility, is uniquely vulnerable to rate increases in an environment of simultaneously rising input costs and decelerating consumer demand.

The poor pay most invisibly and most completely. The poorest Mauritians have no savings, no property, no equity. They have wages. Their wages are suppressed by the imported labour mechanism that keeps the minimum wage floor from rising with productivity. They spend the highest proportion of their income on food and fuel — both of which are rising because of the Iran war oil premium. They receive no benefit from the rate hike while bearing its full cost through reduced credit access, higher prices for everything financed by debt in the supply chain and the knock-on effects of reduced government fiscal capacity for the social services they depend upon most heavily.

The rate hike defends the rupee for everyone in principle. It punishes the middle class through higher mortgage costs, stalls the small business through higher loan rates, deepens the fiscal deficit through higher debt servicing and leaves the poor with higher prices and lower public services. It cannot fix the cause. It redistributes the cost of a war Mauritius did not start.

supply side inflation monetary policy mismatch Mauritius Iran war oil price Hormuz rate hike cannot fix

The Bank of Mauritius cannot be blamed for deploying the instrument available to it. The MPC has a mandate to maintain price stability and orderly economic development. The tools available to a central bank are interest rates, reserve requirements and foreign exchange intervention. When inflation rises from an external supply shock, a central bank can use these tools to manage the domestic transmission of that shock, specifically through exchange rate stabilisation. This is what the rate hike does. It is the appropriate use of an available instrument in response to an external pressure.

What the rate hike cannot do is address the structural vulnerabilities that make Mauritius so acutely exposed to external supply shocks in the first place. It cannot build the strategic petroleum reserve that would have cushioned the Iran war oil premium over a 90-day buffer. It cannot repair the water pipes losing 50 per cent of supply. It cannot build the Rivière des Anguilles dam first promised in 2009. It cannot train the specialist doctors Mauritius must evacuate patients to India to access. It cannot reduce the import dependency that makes every external price shock an immediate domestic crisis. These structural vulnerabilities are not within the central bank's mandate to address. They are within the government's mandate to address. And the government's response to the same external shock that motivated the rate hike has been documented throughout this edition of The Meridian: energy inspectors raiding Tribeca Mall to turn off LED screens, a Price Stabilisation Account in Rs3.2 billion deficit and a water reservoir falling toward 22 per cent capacity.

The rate hike is the monetary system doing what it can. The structural problem is the non-monetary system not doing what it must. The middle class pays the bill for both. The question The Meridian has been asking all month remains unanswered by the MPC statement of 20 May 2026: what is the published plan for building the structural resilience that would make the next external shock less devastating than this one? The rate can be raised. The rupee can be defended. The inflation can be partially contained. But without a strategic petroleum reserve, without domestic food production investment, without renewable energy infrastructure and without the water and health infrastructure that a resilient small island state requires, Mauritius will face the same bill from the next war, the next supply shock and the next external crisis that no interest rate decision can prevent.

Add comment

Comments