How Economic Dependence Entered the Mauritian Home

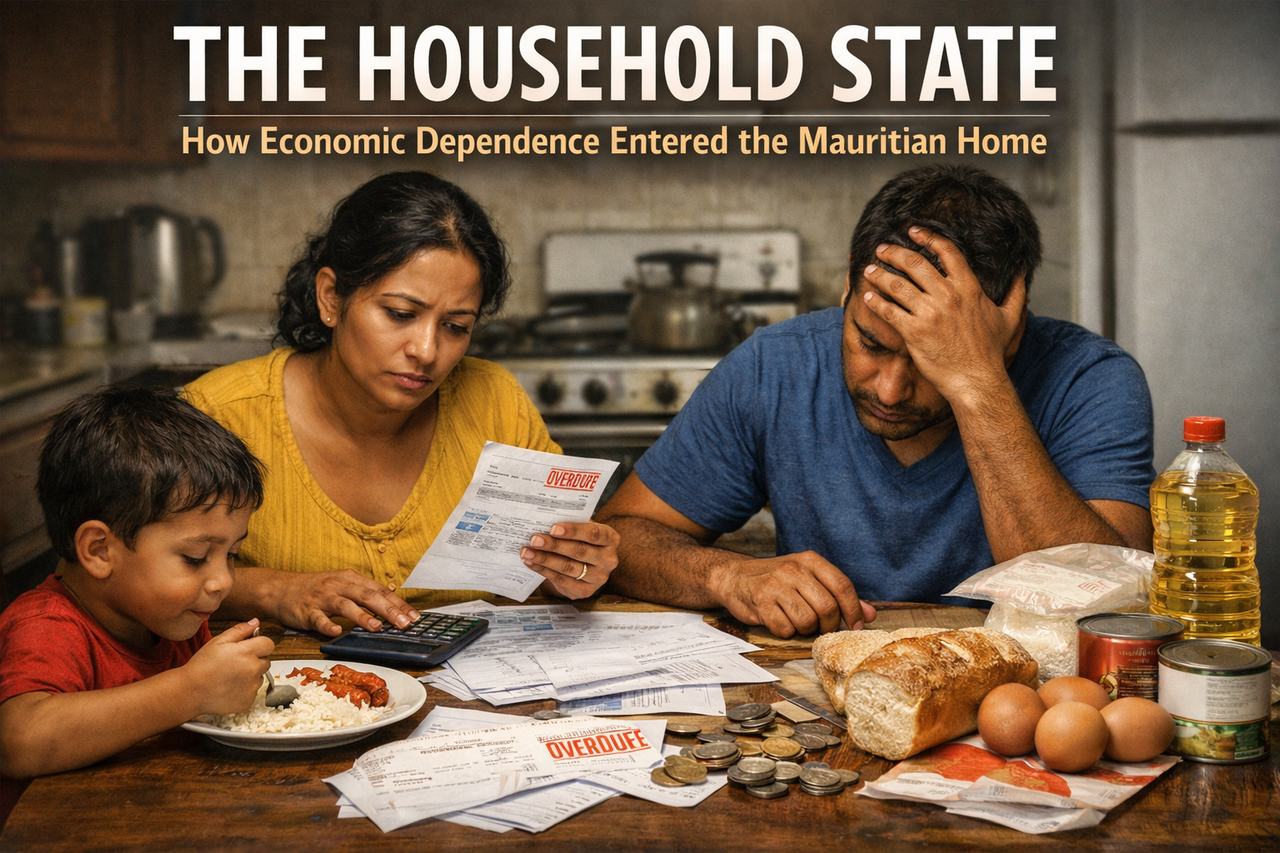

Economies are described through sectors, ministries and aggregate indicators. But in the end, they are judged somewhere more intimate: at the kitchen table, at the rent deadline, in the supermarket aisle, in the moment when wages arrive and disappear. That is where the Mauritian economy now reveals one of its deepest and least comfortable truths. Structural dependence did not remain in the abstract. It entered the home, item by item, month by month, in the gap between what things cost and what wages provide. The great success story of Mauritian economic development, told in GDP growth rates, export diversification and financial sector depth, has a shadow side that those aggregate numbers consistently fail to capture. That shadow side is the Mauritian household, carrying the residual burden of every structural weakness the economy did not resolve at the level of sectors, policy or fiscal architecture.

The Mauritian household has become the final absorber of national vulnerability. Imported inflation, exchange-rate pressure, high food costs, housing strain and weak wage depth no longer sit only in macroeconomic charts. They define the daily structure of family life: what is bought and what is deferred, what is eaten and what is skipped, whether the rent is paid in full or negotiated in arrears, whether the young adult stays in the family home for another year or whether independence can finally be afforded. This is the central argument of this article. Mauritius did not eliminate vulnerability through diversification. It privatised vulnerability into the household budget and then partially socialised the resulting pain through state transfers, wage support and fiscal intervention. The result is a new institutional formation: the household state, in which family survival depends not only on work and savings, but on a complex architecture of public subsidy, administered pricing and managed credit that the state must perpetually maintain at rising fiscal cost.

The numbers behind this architecture are not hidden. The government has been running a fiscal deficit estimated at 9.3 percent of GDP, with public debt at 86.5 percent of GDP against a statutory ceiling of 60 percent. Social assistance, compensation mechanisms and support schemes collectively absorb a significant share of public expenditure. Private-sector credit grew at 11.4 percent in December 2025, signalling that households and businesses alike are relying on borrowing to bridge the gap between income and the cost of normal life. These are not incidental numbers. They are the quantified expression of a household state: a republic in which the family is kept functional by a combination of wages, debt and public subsidy that the state can afford to maintain only by exceeding its own fiscal limits.

The great illusion of macroeconomics is that household life merely follows national economic outcomes in a straightforward transmission from policy to welfare. In Mauritius, the household does considerably more than follow. It absorbs, defers, compensates and quietly restructures its own consumption to accommodate what the wider economy cannot resolve at the level of wages, prices or productive depth. When imported costs rise because the rupee has weakened or global freight has become more expensive, the household does not get a fiscal transfer that perfectly compensates the loss. It adjusts: buying less protein, delaying the car repair, extending the school uniform for another term, choosing the cheaper brand. This adjustment is not recorded in GDP statistics. It is not measured in any official welfare index. But it is the real economy, experienced by real people, every day.

This is why the household has become one of the most important economic institutions in contemporary Mauritius. Not because it has become wealthy, but because it has become the place where unresolved structural dependence is made temporarily livable through private sacrifice and incremental adjustment. The state may stabilise part of the surface through transfers and administered prices. Firms may pass on costs through price increases. External markets may set the rates at which Mauritius imports the fuel, food and goods its households consume. But the final burden, the gap between what things cost and what wages provide, is carried privately inside the family budget, at the kitchen table, in precisely the kind of quiet material stress that official statistics consistently undercount.

Mauritius did not eliminate vulnerability through diversification. It privatised vulnerability into household life, then used the State to delay the moment when that privatisation became socially ungovernable.

Vayu Putra · The Meridian · April 2026Mauritius imports a large proportion of what its households consume, which makes the family kitchen one of the republic's most externally exposed economic spaces. Food costs are highly sensitive to global freight conditions, oil prices, imported input costs and exchange-rate movements. When any of these variables moves against Mauritius, the cost of feeding a family rises without any corresponding domestic mechanism to absorb or offset the increase. The household therefore lives inside a cost structure it did not choose, cannot influence and cannot easily escape.

Headline inflation eased to approximately 3.8 percent by early 2026, down from 10.8 percent in 2022 and 7.0 percent in 2023. That statistical improvement must not be mistaken for relief. A lower inflation rate does not reverse a price shock. It only means that prices are rising from a much higher base at a slower pace than before. The basket that a Mauritian household carries to the supermarket today is materially heavier than the basket it carried in 2020, and the wages with which it fills that basket have not risen proportionately. Real purchasing power for large sections of the Mauritian working and lower-middle class was eroded significantly during the 2022-2023 inflation shock, and much of that erosion has not been recovered. Official figures suggesting an 18.4 percent real wage erosion for the middle class since 2022 are consistent with the lived experience that policy language consistently fails to capture. The daily experience of inflation is not an annual percentage. It is the cumulative heaviness of a basket that demands more each month without wages rising to match.

When the basket gets heavier and wages cannot keep pace, families do not simply consume less across all categories proportionally. They make choices about what to sacrifice first. Protein is often among the first to go. Nutritional quality declines before caloric sufficiency does. The household crisis in Mauritius is therefore not only a budget crisis. It is also, incrementally and invisibly, a food-quality and long-term health crisis whose costs will appear in the health system rather than in household budget statistics.

The statutory minimum wage of Rs 17,745 per month from January 2026 represents the formal floor of what Mauritius has decided a working person should earn as a minimum. That floor matters and the wage has been lifted in nominal terms over recent years. But the structural problem is not the nominal floor. It is the relationship between the floor and what a normal life actually costs on this island in 2026. Housing costs are elevated. Food costs are elevated relative to 2020. Transport costs are elevated. Utility costs have risen with imported energy prices. The minimum wage is a legal protection. It is not, in the experience of families living near it, a guarantee of comfort or stability.

The state's involvement in the wage system goes deeper than setting the legal minimum. Revenue-support mechanisms and compensation arrangements help certain employers meet wage obligations or cushion the impact of energy cost increases on operating costs. This means that part of lower-tier household purchasing power is sustained not purely by private productive activity generating sufficient surplus to pay living wages, but by public fiscal mechanisms compensating for the gap between what the market generates and what the policy framework requires. If the state must help parts of the private sector meet the legal wage floor, then the wage system is no longer purely market-generated. It is partially fiscal. The household income of the lower-wage Mauritian worker is, in this sense, a composite: partly private employer payment, partly state-enabled compensation. That is the institutional reality of the wage floor in the household state.

When wages fail to fully cover the cost of living, and when state transfers fill only part of the remaining gap, credit enters as the bridge. The 11.4 percent year-on-year growth in private-sector credit recorded by the Bank of Mauritius for December 2025 is one of the most important single statistics in understanding the current state of the Mauritian household economy. It tells us that the mechanism through which households and businesses are maintaining their consumption levels and operational continuity is not primarily rising wages or improved productive capacity. It is borrowing.

Credit is often described in the language of confidence: when lending grows, it is presented as a sign of economic optimism and investment appetite. In a society under sustained cost pressure, however, credit growth can mean something structurally different. It can mean survival financed forward: the decision to borrow now in order to maintain normal life now, deferring the adjustment that reduced purchasing power would otherwise impose. A household that increases its personal loan balance to pay for school fees, a medical bill or a consumer purchase it cannot cover from wages is not expressing confidence in the economy. It is expressing the absence of an alternative. The gap between income and cost must be filled by something. When wages and transfers are insufficient, credit fills it. The repayment problem is thereby shifted from the present into the future, where it will arrive as a more concentrated shock rather than a more distributed and manageable adjustment.

Housing costs in Mauritius have been elevated by a combination of land scarcity, premium property development orientated toward foreign buyers and the integrated resort scheme market, and the broader inflation in construction inputs that has affected building costs across the island. Mortgage rates may have eased, with new housing loan rates falling to around 5.49 percent in late 2025 following a period of higher rates. But the primary barrier for most first-time buyers and young households is not the interest rate on a mortgage. It is the entry price of the property itself, which has risen beyond what the wage levels of most working Mauritians can service even at reduced interest rates.

For many younger Mauritians, independent household formation has been delayed not by cultural preference but by economic constraint. The combination of elevated property prices, wage levels that do not generate sufficient savings for a deposit at speed, and the general cost pressure of daily life in an import-dependent economy has made leaving the parental home a longer and more difficult process than it was for earlier generations. This creates pressures that appear nowhere in the national accounts: extended family dependence, crowded housing, delayed family formation, reduced privacy and the social and psychological costs of an adulthood that is economically deferred. These are the real-world consequences of an economy that has managed its housing and land use with insufficient attention to the needs of its domestic population as distinct from the preferences of its international property investors.

Female labour-force participation in Mauritius remains around 47 percent, a figure that is low by comparison with upper-middle-income economies of comparable development status. The policy and social reasons for this are complex and contested. But from the perspective of household economics, the consequence is clear and structurally significant: a large share of Mauritian households is trying to sustain a 2026 cost structure on a single primary income. In an economy where the cost of food, housing, utilities, transport, school fees and healthcare has risen substantially over the past four years, the single-income household carries a materially narrower margin for absorbing shocks than the dual-income household that can draw on two earnings streams when one is disrupted.

The more expensive and import-exposed daily life becomes, the more the second income shifts from a lifestyle aspiration to a structural necessity. Where that second income is absent, whether because of caring responsibilities, labour market barriers, wage levels too low to justify the cost of childcare, or other structural factors, the household is left more exposed to every cost increase, every job disruption and every unexpected bill than official household income statistics typically capture. This is one of the quiet structural vulnerabilities running through the Mauritian social economy: the architecture of household income has not kept pace with the architecture of household cost.

The fiscal state now sits inside Mauritian household survival considerably more deeply than the public political narrative typically acknowledges. Social assistance programmes, pension transfers, the basic retirement pension, compensation schemes tied to fuel and food prices, wage-support mechanisms and related fiscal interventions are not peripheral spending lines in the national budget. They are part of the core architecture through which domestic life in Mauritius remains economically governable. Without them, the gap between wages and costs would produce visible social stress at a scale that the political system could not absorb without significant disruption.

This does not make these interventions wrong. On the contrary, they are socially necessary and politically indispensable in an economy whose structural dependence has been transferred into household budgets without being resolved at the source. But it does mean that the Mauritian household is not primarily sustained by the private wage economy's productive capacity. It is sustained by a combination of private earnings, household debt and a state apparatus spending significantly more than its fiscal rules permit. The fiscal deficit of 9.3 percent of GDP and the public debt ratio of 86.5 percent against a 60 percent statutory ceiling are not only macroeconomic problems. They are the quantified cost of maintaining the household state: the bill for preventing private social collapse in an economy that has not generated sufficient domestic productive depth to sustain its own households through private activity alone.

The government is no longer only the manager of the Mauritian economy. In important and largely unacknowledged ways, it has become a hidden co-provider inside the Mauritian household. And it is a co-provider whose own fiscal position is deteriorating at the same rate as the households it supports need more from it.

Vayu Putra · The Meridian · April 2026The household state is the institutional formation that emerges when national economic dependence moves through prices into homes, and when the state then re-enters the home through transfers, wage engineering, administered pricing and fiscal cushioning in order to prevent the social consequences of that dependence from becoming politically ungovernable. It is a system in which the family carries the immediate burden of imported inflation, wage inadequacy, housing cost and daily economic stress, while the state carries the deferred and accumulated burden of compensating for a model that does not generate sufficient domestic productive surplus to sustain its own population through private activity alone.

This is not stable equilibrium. It is a holding pattern with a deteriorating fiscal foundation. Mauritius has reached a point where household survival can no longer be explained primarily by work, thrift or family discipline. The problem is structural. The island imports too much of daily life at prices it does not control. It generates wages too shallow to cover those import costs without supplementation. It prices land and housing in ways that progressively exclude the domestic population. It relies increasingly on credit and public transfer to bridge the growing gap between what private economic activity generates and what a functioning household requires. The state absorbs what the economy does not produce, and it does so at a rate that is pushing its own fiscal position beyond the limits its laws set for it.

The household does not merely live inside the Mauritian economy anymore. It now carries the unresolved contradictions of that economy in its own budget, at its own kitchen table, in its own daily arithmetic of what can be afforded and what must be deferred. That is what the household state looks like from the inside.

This article examines how structural dependence in Mauritius finally lands in domestic life: through food, wages, debt, housing cost, delayed adulthood and the growing role of the State in household survival. It is part of The Meridian's extended Pillars of Dependence investigation into the accumulated cost of the Mauritian economic model.

Its central argument is that Mauritius did not eliminate vulnerability through economic diversification. It transferred vulnerability into household life, then used public fiscal resources to manage the resulting pressure, at a cost the State can no longer comfortably afford.

The Mauritian household is now the place where the republic's economic contradictions are finally paid for in full. Imported inflation enters through the food bill and the fuel pump. Wage weakness enters through the gap between what work pays and what life costs. Land and housing pressure enter through delayed adulthood and extended family dependence. Credit enters as compensation: the debt that bridges the gap between income and the cost of maintaining normal life. The state enters as the hidden co-provider: the fiscal apparatus absorbing what private economic activity cannot generate, at a deficit it can no longer afford and a debt level it has already exceeded by law.

This is not a description of a society in collapse. Mauritius is not collapsing. Its institutions function, its economy grows, its people are resilient and its social fabric remains comparatively strong. But it is a description of a society carrying a structural burden that grows heavier each year because the economic model that generates the burden has not been fundamentally reformed. The household absorbs what the sectors do not resolve. The state absorbs what the household cannot carry alone. And the fiscal cost of that absorption compounds at a rate that the next generation will inherit in the form of debt, pension liability and a public balance sheet whose capacity to continue cushioning private household stress is already constrained by its own legal limits.

The Pillars of Dependence that this series has examined across sugar, tourism, textiles, offshore finance and the blue economy all share a common endpoint: the Mauritian household. That is where the external price, the imported input, the externally determined wage condition and the unresolved structural vulnerability eventually land. Understanding the household state is not a supplement to understanding the Mauritian economy. It is, in the end, the point of the whole analysis.

April 2026 · Political Economy · Mauritius Investigation